Oil giveth and taketh away

1) Last quarter’s oil price drop subtracted 0.5%-pt (ar) from 3Q headline CPI and boosted consumer spending

2) With oil at $80/bbl, the beneficial effects of this purchasing power boost are set to fade this quarter

3) Impact varies across countries depending on government interventions in retail prices

4) Higher oil, along with less supportive US financial conditions, could constrain easing cycles in some EMs

Tensions in the Middle East drove crude oil prices higher in recent weeks, raising concerns that this shock could boost inflation and dampen global growth. The oil price rise so far is relatively modest by historical standards, but geopolitical uncertainty remains high and the rise comes after a quarter in which a larger-than-expected oil price drop supported consumer real incomes and spending. Assuming oil prices settle around $80/bbl, inflation is likely to pick up again in coming months. The associated global growth drag, while likely modest, would reverse some of the recent support for consumers.

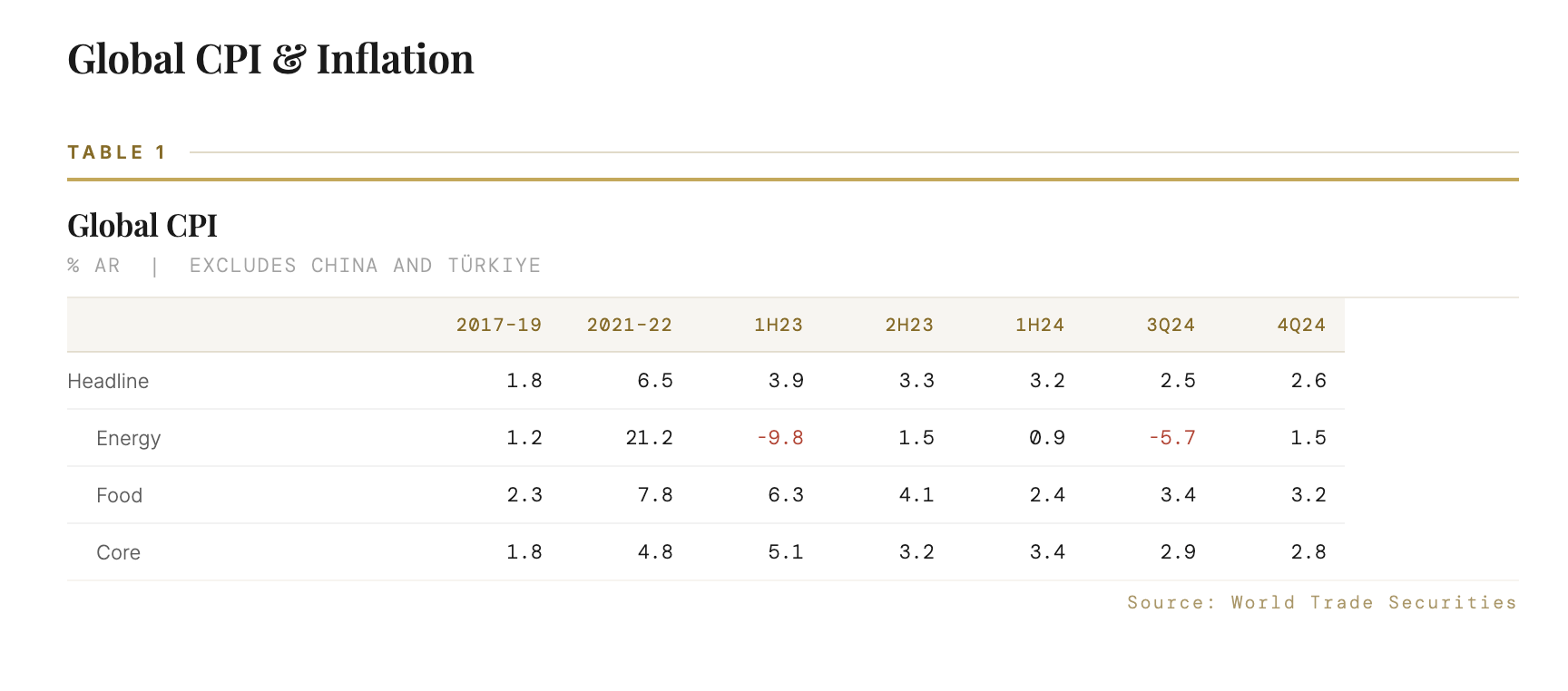

The pass-through from oil prices to consumer prices is relatively quick although it varies by country. From a peak of 9%ar in the three months to April, the global energy CPI swung to -4% in August and the drop looks to have intensified in September. While oil prices are still around 5% below July levels, this month’s jump has erased September’s decline and the increase should pass through to consumer prices with a modest lag. We estimate that a Brent crude average of $80/bbl, in line with our commodity research team’s forecast, would lift the energy CPI back up to a 8%ar in the three months to December.

The relationship between inflation and crude oil prices weakened post-pandemic as headline inflation jumped to 9%ar in response to a broad-based commodity price surge and supply chain dislocations. But since a fading of these shocks returned inflation close to 3%ar in mid-2023, oil prices have again become more closely aligned with headline inflation swings. We expect the swing higher in the energy CPI this quarter will push headline inflation back up to 3.2%ar in the three months to December–– a swing that would nonetheless leave headline inflation on course to moderate to a 2.6%ar in 2H24 from 3.2% in 1H24.

Assessing the impact of oil price swings on growth is less clear and depends on whether the move owes to a supply or demand shock. To the extent that higher oil prices reflect stronger demand, the rise in oil prices is associated with an improvement in growth. But if oil prices rise due to reduced supply, it is a net drag on demand. Both our commodity strategists’ and the latest data on global demand suggest the 3Q oil price drop owed to stronger supply, while low level of oil inventories point to a fair value of $80/bbl in 4Q24.

Based on our analytic global oil supply-demand model, a supply induced 10% rise in oil price damps global GDP by 0.16%. Assuming this impact is concentrated over two quarters, the drag on annualised GDP growth is 0.32%-pt. Again, the growth impact is felt differently across countries depending largely on whether they are net oil exporters or importers. We explore these variations in the sections below.

Energy CPIs down, but also complicated

As a rule of thumb, a 10% change in the oil price moves global headline CPI by 0.2%-pt (0.4%-pt ar over two quarters). However, the pass-through is felt differently across countries and depends in part on how fiscal policies are used in response to a change in the oil price. The use of fiscal interventions in fuel prices through indirect taxes and subsidies have historically tended to be larger in EM than DM.

In the 2015 oil price tumble many EMs did not pass the full decline in global crude price to the retail level. Instead, governments increased excise taxes to boost public finances and reduce current account deficits. Similarly, in the recent phase of falling oil prices, some EMs unwound fuel subsidies to reduce fiscal deficits. This limited the impact on both inflation and consumer incomes and spending. DM price interventions also gained traction since the pandemic; much of the Euro area used fiscal subsidies to mitigate the pass-through from the 2022 natural gas price surge to consumers. Japan has also intermittently subsidised domestic utility bills.

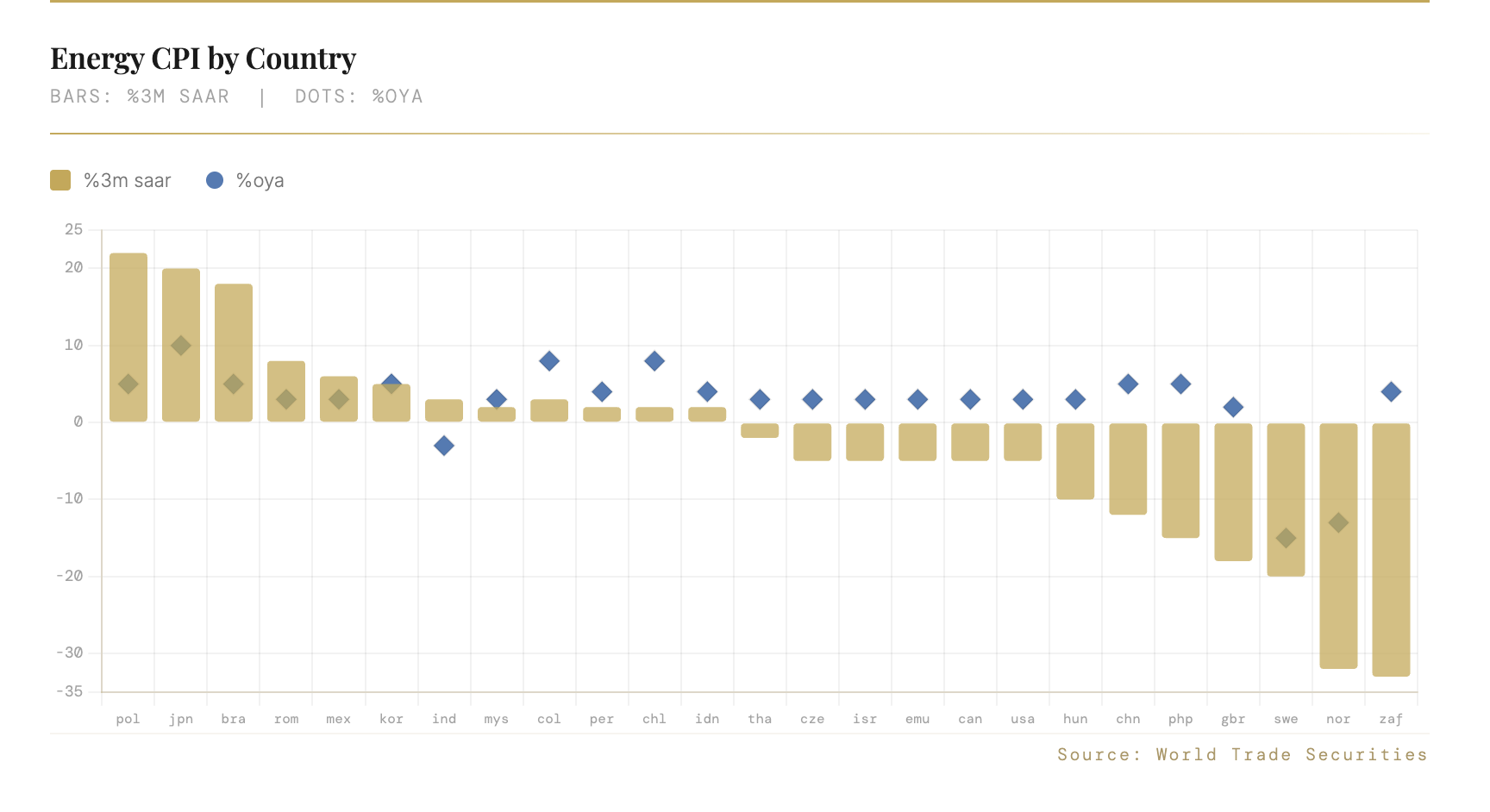

Given the varied mechanisms for adjusting retail prices, it is not surprising to see a significant dispersion in CPI dynamics. Indeed, in the last three months only about 60% of the 30 countries we follow reported a decline consumer energy prices. We discuss these variations in more detail in the next sections. The steeper declines in the UK and Scandis–– and the jump in Poland and Japan––reflect changes in domestic energy utility bills.

Crude not the only game in town

The change in crude oil prices can be either reinforced or offset by changes in other energy prices. Motor fuels, which tend to co move most closely with crude oil prices, make up only about half of energy prices in consumer baskets. The rest comprises domestic energy utilities/services; these respond more to region-specific natural gas and/electricity prices and may or may not co-move with oil prices.

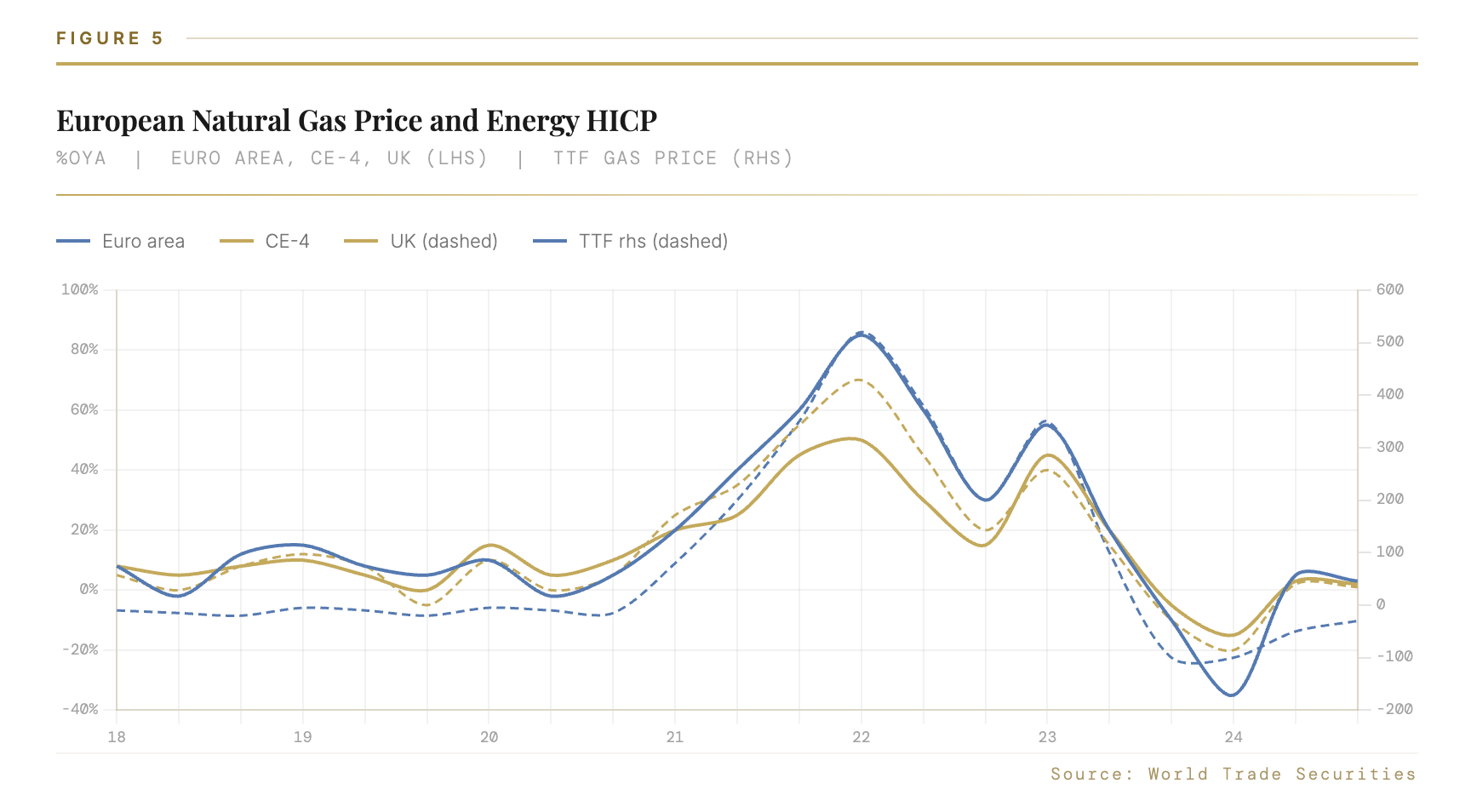

Wholesale natural gas prices are well off their 2021-22 peaks but have been rising again of late (Figure 4). Gas prices have played the biggest role in Europe’s inflation dynamics both due to the magnitude of the swings and the larger weight of energy utilities in retail prices. European natural gas prices (TTF) are up 36% in the past six months but this is a relatively small move compared to recent years and the region’s lumpy and varied response to the 2022 natural gas price surge looks to be largely complete. As a result, assuming domestic utility bills remain unchanged, the region’s energy CPI is likely to remain close to -5%ar this quarter.

In the US, falling gasoline prices pushed energy CPI down 10%ar in the three months to September to deliver substantial relief to US household’s purchasing power last quarter (Figure 6). However this month’s rebound is already passing through to retail prices and should lift the energy CPI back into positive territory in 4Q––a rise that could get an added kick from the jump in US natural gas prices in recent months.

Asian natural gas (LNG) spot prices are up 30% in the past six months but the region’s household utility prices are largely linked to crude oil prices and household energy prices outside of China and a few other countries continue to be heavily subsidised by governments. Japan’s energy CPI is up sharply, but a re-introduction of electricity and gas price subsidies should bring it lower this quarter.

Varied country sensitivities to oil

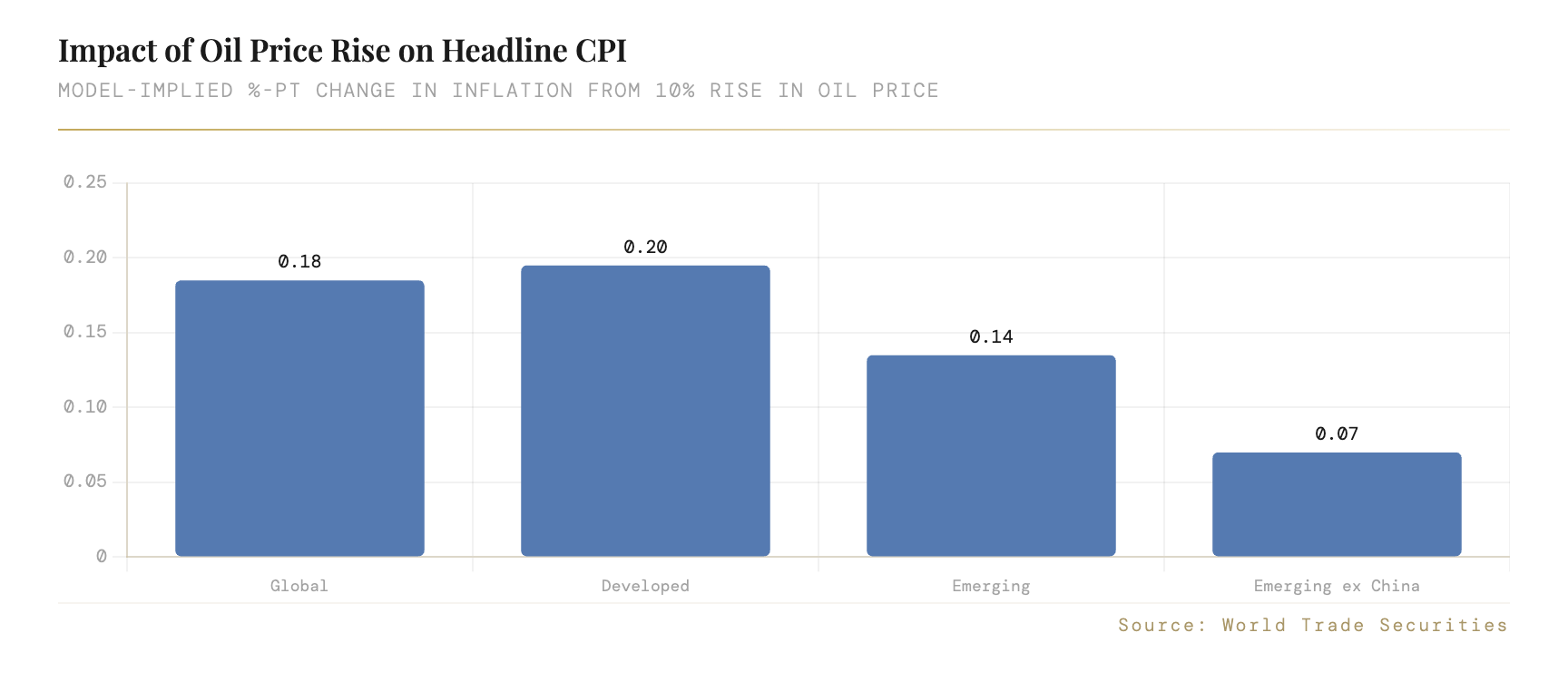

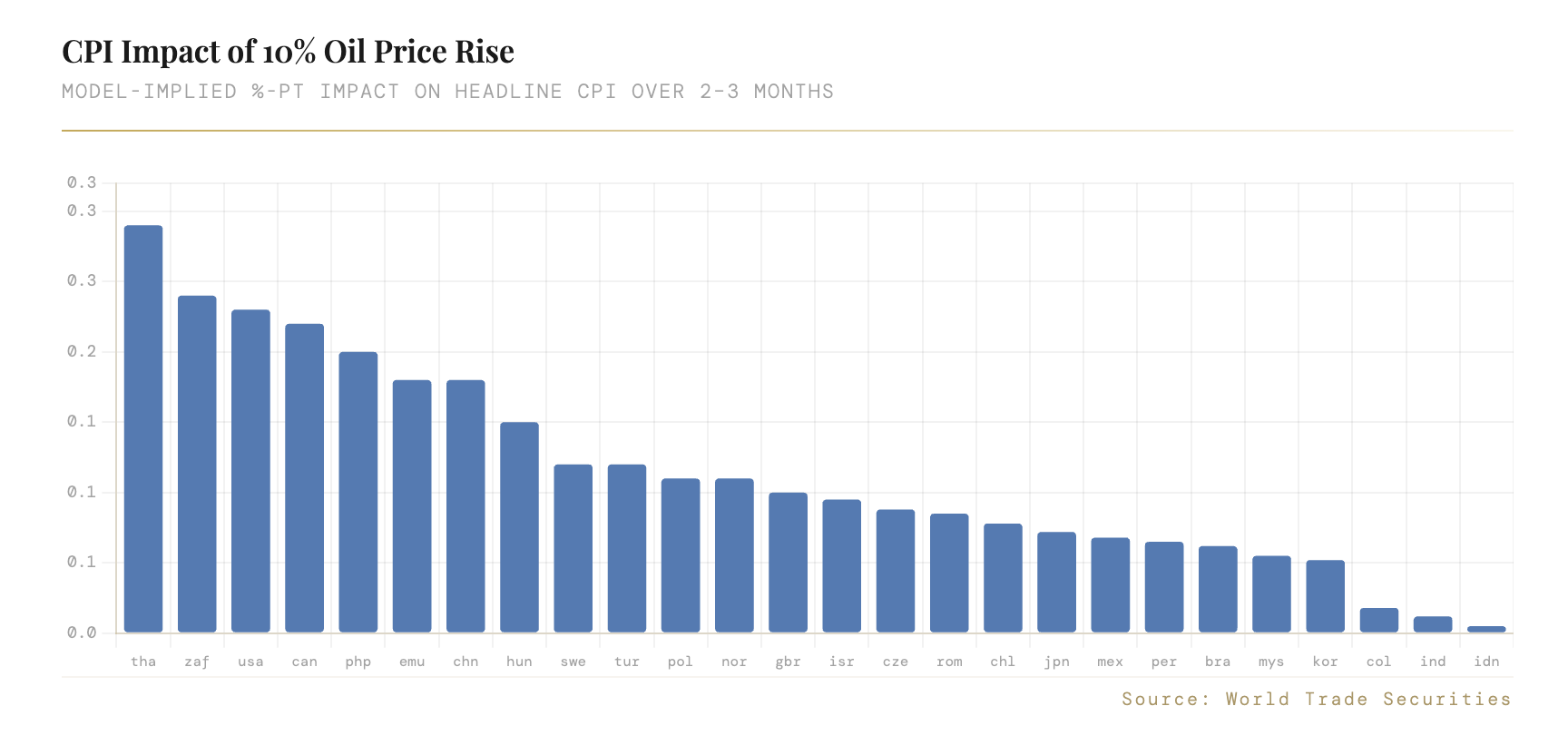

Next we explore the relationship between oil prices and CPI more formally based on the historical relationship across our sample of 30 countries. Specifically, we regress %m/m changes in each country’s energy CPI on current and lagged Brent crude oil (allowing up to two lags where significant) since the mid-2000s. We then scale the model-based response: i) by each country’s respective energy weight in the CPI, and ii) the magnitude of the oil price change (i.e.; 10%). This impact, which excludes potential pass-through to core inflation, is shown in.

– In EM, the largest estimated impacts are in Thailand, South Africa, Philippines, China and Hungary. While EM Asian countries have gradually dismantled energy price subsidies, subsidies are still material in Indonesia, India and Malaysia making domestic retail prices much less sensitive to movements in global crude oil prices. In Poland and Czechia, energy utilities account for a larger share of consumer baskets than motor fuels.

– In Latam, the model-implied impact of 0.1%-pt is relatively small largely due to widespread government controls. In Brazil, Petrobras sets domestic gasoline prices and electricity prices rely on hydroplants, limiting the sensitivity of energy prices to global prices. In Mexico, consumer energy prices are controlled except natural gas which has a small weight and the sensitivity tends to be asymmetric due to tax policy.

– Among DMs, the US, Canada and Euro area are likely to feel the impact the most strongly as every 10% move in oil prices raises headline by 0.3%-pts. Where the impact is more muted, a high share of fixed costs (including excise taxes, subsidies and network/distribution costs) in consumer prices or a larger share of regulated prices in energy bills are likely responsible. For instance in Japan, motor fuels account for only 1.8% of the CPI.

The growth impact is likewise felt differently across countries, depending on crude oil intensity and whether the country is a net oil importer or exporter. While higher oil prices (owing to a supply shock) lead to stronger growth in oil producers––either through higher oil production or increases in government spending––the drag on oil importers more than offsets this impact at the global level.

In DM, the largest net energy importers are the Euro area, UK and Japan, but higher oil prices also damp US growth given its high energy intensity. In EM, we estimate a 0.1%-pt GDP drag on EM Asia where all countries except Malaysia are net oil importers. In EMEA EM, the largest drags are on Turkey and CEE (especially Hungary). LatAm shows a negligible overall GDP response as the region overall has a roughly neutral oil trade balance.

A modest boost to 4Q CPI, drag on GDP

Most of the 3Q crude oil price decline should have passed through to consumer prices already in September and we look for consumer energy prices to rise a cumulative 2% over October-November. This should push headline CPI gains up to around 3% on a 3m saar basis by December. The pick-up in year-ago CPI rates should be further boosted by base effects as energy prices fell sharply in the last quarter of 2023. In all, after falling to its lowest since 2021 in September, we forecast headline inflation should rebound to 3%oya by year-end.

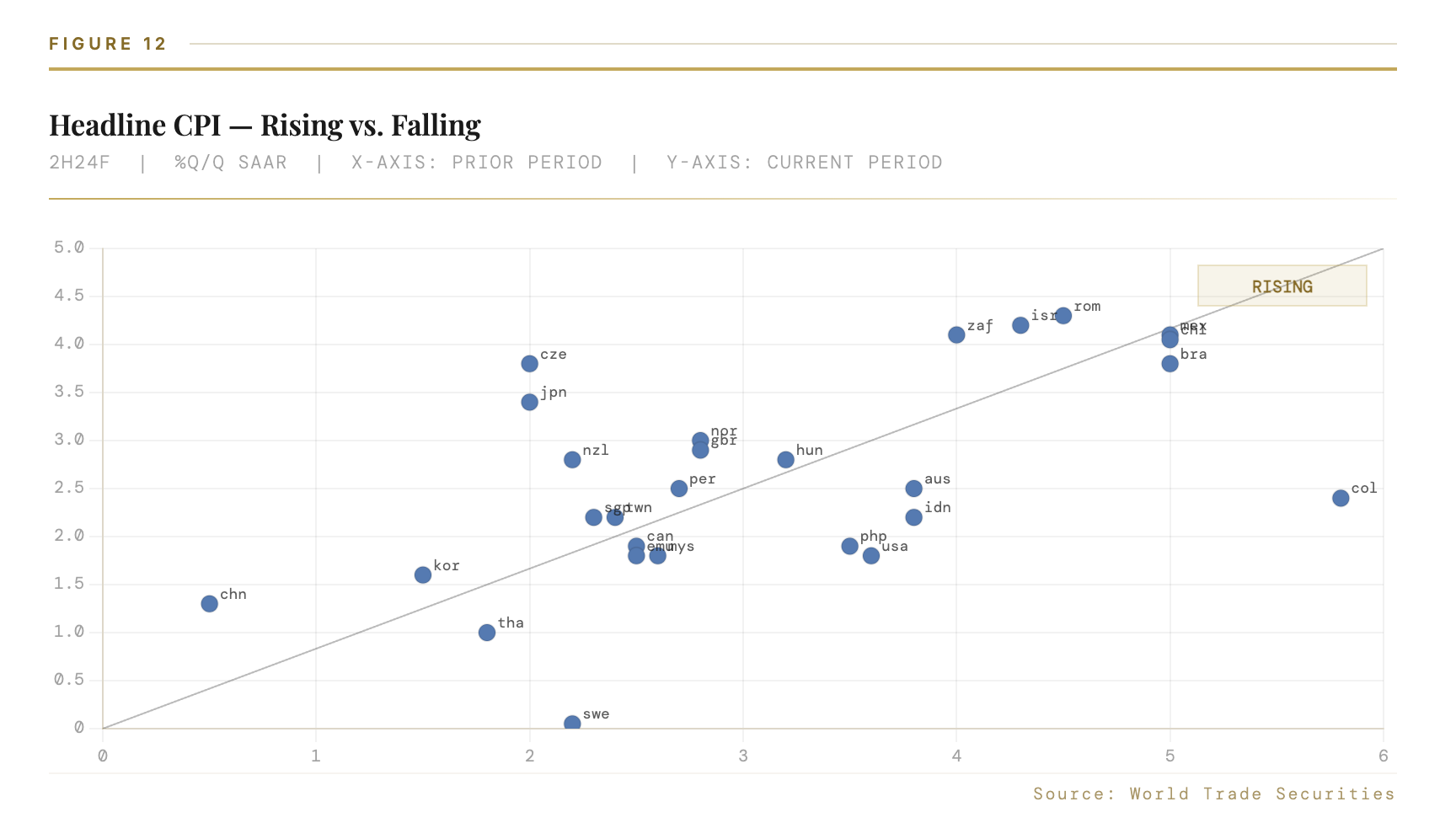

The country level variation is again large but, on the whole, a majority of countries (60%) are still likely to see headline inflation rates ease in 2H4 relative to 1H24 (Figure 12).In the DM, the US is expected to see one of the largest declines with headline CPI gains easing from 3.3% in 1H24 to 1.7%ar in 2H24, only outdone by Sweden where a 2%-pt drop is expected to push headline inflation close to 0%ar. In EM, the most pronounced headline inflation declines are in Turkiye, Colombia, Indonesia and the Philippines.

EM CBs a bit more constrained

Policymakers in DM will look through the 2H swings in headline inflation, particularly if they view changes in oil prices as driven by supply shocks. Historically, there has been limited pass-through from oil price movements into core inflation. To the extent there is a positive relationship sustained swings in underlying demand are the likely reason. Our base case sees only a limited moderation in core inflation to a 2.8%ar in 2H24. If oil prices decline and the drop is accompanied by a broader softening in underlying inflation, central banks could accelerate their easing, particularly if downside growth risks magnify.

For EM central banks, front-loaded Fed easing and the fall in energy prices in 3Q provided space for more front-loaded cuts, especially in parts of EM Asia and South Africa, where inflation has already returned to central bank targets. A rebound in oil prices this month, along with a re-assessment of Fed easing and a stronger dollar, removes some of these tailwinds and could temper the pace of easing cycles in some countries. This argues for greater near-term CB caution in countries that are more sensitive to external financial conditions such as EM Asia, Mexico and South Africa.

General disclosures: This research is for our clients only. Other than disclosures relating to World Trade Securities, this research is based on current public information that we consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. The information, opinions, estimates and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large majority of reports are published at irregular intervals as appropriate in the analyst’s judgment. World Trade Securities conducts a global full-service, integrated investment banking, investment management, and brokerage business. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and principal trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, principal trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this research. We and our affiliates, officers, directors, and employees will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any, referred to in this research, unless otherwise prohibited by regulation or World Trade Securities policy. The views attributed to third party presenters at World Trade Securities arranged conferences, including individuals from other parts of World Trade Securities, do not necessarily reflect those of Global Investment Research and are not an official view of World Trade Securities. Any third party referenced herein, including any salespeople, traders and other professionals or members of their household, may have positions in the products mentioned that are inconsistent with the views expressed by analysts named in this report. This research is focused on investment themes across markets, industries and sectors. It does not attempt to distinguish between the prospects or performance of, or provide analysis of, individual companies within any industry or sector we describe. Any trading recommendation in this research relating to an equity or credit security or securities within an industry or sector is reflective of the investment theme being discussed and is not a recommendation of any such security in isolation. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments. Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Investors should review current options and futures disclosure documents which are available from World Trade Securities sales representatives.

© 2023 World Trade Securities. No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The World Trade Securities L.P team.