– Both Trump and Vance have voiced support for a weaker dollar policy

– The president has legal avenues to attempt to depreciate the dollar, though only limited resources to do so

– There are also doubts about the effectiveness of those avenues if monetary policy remains independent

A recent Bloomberg Businessweek interview with Republican presidential nominee Trump began with an open-ended question: “What kind of economy do you want for the American people in terms of innovation, opportunity and global competitiveness?” Trump answered “Well I think manufacturing is a big deal, and everybody that runs for office says you’ll never manufacture again. We have currency problems, as you know. Currency.” From there he spent the next two paragraphs discussing the problems with dollar strength, yen weakness, and, particularly, yuan weakness.

The topic of dollar strength is clearly top of mind for Trump, and his running mate J.D. Vance has also voiced his desire for a cheaper dollar. Many commentators have pointed out that Trump’s wish to depreciate the dollar is at odds with his trade policy preferences, as theory predicts that the currency of a tariff-imposing country should appreciate following higher import duties. That complication doesn’t necessarily mean that a Trump administration wouldn’t pursue policies to weaken the dollar.

In this note we look at the tools the executive branch has in the realm of currency policy. We also describe the evidence on the effectiveness of sterilized intervention, concluding that intervention against other major currencies such as the euro or the yen is unlikely to be very effective. However, it could be more effective—or at least disruptive—if it was targeted at smaller countries, particularly those that intervene to weaken their currency.

Currency war redux

The simplest way to reduce the exchange value of the dollar is for the Fed to act more dovishly. As we discussed last week, we think that at least initially, the Fed under a second Trump presidency would remain focused on the dual mandate and would not pursue a weaker dollar as an end in itself.

Even so, the executive branch has other tools with which to conduct dollar policy independent of Congress or of other independent agencies like the Fed. The Gold Reserve Act of 1934 created the Exchange Stabilization Fund (ESF). Initially seeded with $2 billion, retained earnings have allowed the ESF to grow to $215 billion over the subsequent 90 years. This fund is “under the exclusive control of the Secretary of the Treasury, with the approval of the President, whose decisions shall be final and not be subject to review by any other officer of the United States.” Moreover, one of the motivating considerations for the creation of the ESF was to prevent dollar appreciation (particularly vis-à-vis the pound). Thus, there should be little doubt the president can use the resources of the ESF to try to weaken the dollar.

The situation is somewhat more ambiguous when it comes to the Federal Reserve’s partnership. The Fed has two roles in US currency policy. First, Treasury interventions are executed by the Federal Reserve Bank of New York. Second, since 1961 the Fed has traditionally matched Treasury intervention funds on a dollar-per-dollar basis. This effectively doubles the ESF’s potential resources. (Though this still leaves those resources quite limited by international standards; a larger ESF would need Congressional approval).

Since then, members of the FOMC have occasionally chafed at partnering with Treasury in currency interventions. This discontent increased in the late 1980s and early 1990s as the economics profession began questioning the efficacy of such interventions (more on this below). The tension has since been defused by the simple fact that Treasury and the Fed have intervened only a handful of times since the mid-1990s. Were the current Treasury to re-engage the currency markets in one form or another, the Powell Fed might fall in line and follow the traditional post-1961 policy, particularly if it received tacit Congressional support for such action. Failure to cooperate with Treasury could bring unwanted political attention at a delicate time for the Fed. Moreover, even a large intervention would be a blip on the Fed’s roughly $7 trillion balance sheet.

How effective?

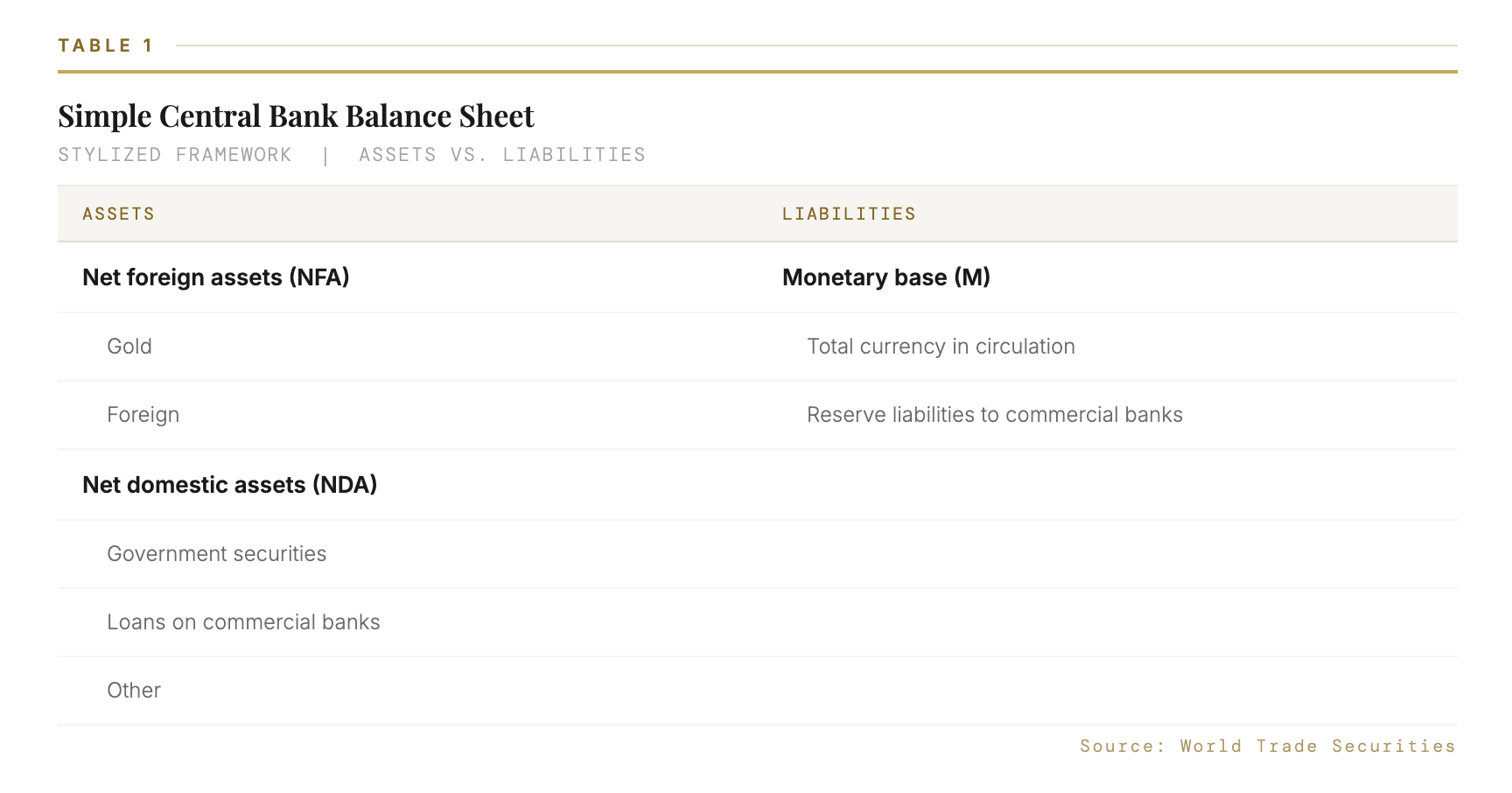

To consider whether such an intervention would be effective we first step back from looking at institutions to focus on economics. Intervention refers to transactions in foreign exchange undertaken by the official sector to influence the foreign exchange rates. Intervention comes in two forms: unsterilized and sterilized. To understand the difference, we first depict a simplified central bank balance sheet in

The simpler case is unsterilized intervention, when the central bank purchases (or sells) foreign assets, with no other offsetting transactions. As a result the monetary base increases (decreases) which in turn lowers (raises) short-term interest rates. Interest parity relations then imply in equilibrium that the value of the domestic currency decreases (increases). There is little question, theoretically or empirically, that unsterilized intervention impacts the foreign exchange value of the currency.

Sterilized intervention is an attempt to insulate domestic monetary conditions from foreign exchange intervention by conducting equal but opposite transactions in domestic assets. For example, a sterilized attempt to depreciate the currency would involve purchases of foreign assets and sales of domestic assets. In terms of Table 1, sterilized intervention would involve ∆NFA=-∆NDA which implies that ∆M=0. However, if the monetary base doesn’t change then domestic short-term interest rates won’t change. Note that since 2008 the Fed has set interest rates not by changing the monetary base M, but rather by adjusting administered interest rates, primarily IOER. What this means is that in the current institutional setting any intervention by US authorities will be sterilized intervention—i.e., it won’t directly affect short-term interest rates.

The effects of sterilized interventions are debated. If domestic and foreign interest rates don’t change—as is the case in sterilized intervention—then there is no reason to expect exchange rates to change. At least, that is what economic theory suggests, and is why the effectiveness of sterilized intervention came into doubt in the 1980s. Theory doesn’t stand still, however, and a few extensions have been offered for why sterilized interventions can matter. The first is the portfolio balance mechanism. According to this view, investors have a desire for a certain mix of domestic and foreign assets. If the central bank, say, buys foreign assets this would reduce the supply of those assets available to investors, who would bid them up, putting upward pressure on the value of the foreign currency. Another means by which sterilized intervention might affect exchange rates is the signaling channel. If an intervention is seen as a signal of the future direction of monetary policy then the price of foreign exchange which is a forward-looking asset price—should respond to such interventions.

The empirical evidence on the effectiveness of sterilized intervention is mixed, though with the evidence leaning on the side of sterilized interventions having some modest effect on exchange rates. Generally more meaningful effects are found to occur when the intervention is (i) publicly announced—consistent with the signaling channel view—and (ii) coordinated with foreign monetary authorities. The signaling channel is less likely to be effective if the Fed is viewed as independent in the realm of interest rate policy. Moreover, the latter stipulation—coordinated intervention—is unlikely to pertain if the US decides to attempt to weaken the dollar. These two limitations would seem to be particularly challenging if the US were to attempt to weaken the dollar against other major freely floating currencies.

A different policy option more narrowly focused on countries that arguably intervene to weaken their currency (e.g., Malaysia, Singapore, etc.) would be to conduct “countervailing currency intervention.” The gist of this policy would be to purchase, say, ringgit by issuing dollars to offset Malaysian purchases of dollars financed by ringgit creation. The intent would be to neutralize the impact of Malaysian intervention on the exchange rate between the two currencies.

The elephant in the room is China. One obvious problem with this policy of countervailing currency intervention against China is that China maintains capital controls such that any potential intervention by the US would need to be undertaken in the offshore CNH market. However, the PBOC, through regulatory and other means, can sustain a wedge between the two markets if it so desires. Of course, such actions come at a cost, including raising questions about China’s declared aim to internationalize the use of its currency. Separately, there is the question of whether there are enough international renminbi assets available to purchase, but in any case, would be unlikely to be enough to materially move China’s monetary policy. In addition to these challenges, this policy would raise market uncertainty and could provoke countermeasures from the Chinese that, in turn, increase the risk of unintended consequences.

The mainstream of the economics profession has considerable reservations about the effectiveness, or even harmlessness, of unilateral intervention aimed at weakening the dollar. Even so, that’s no reason to rule it out as an option the administration might consider.

© 2023 World Trade Securities. No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The World Trade Securities L.P team.