Euro area: Making progress on disinflation

– Recent slowing in core inflation is linked to services

– Deflator down sharply; wage inflation should fade

– We continue to expect core inflation to return to 2%

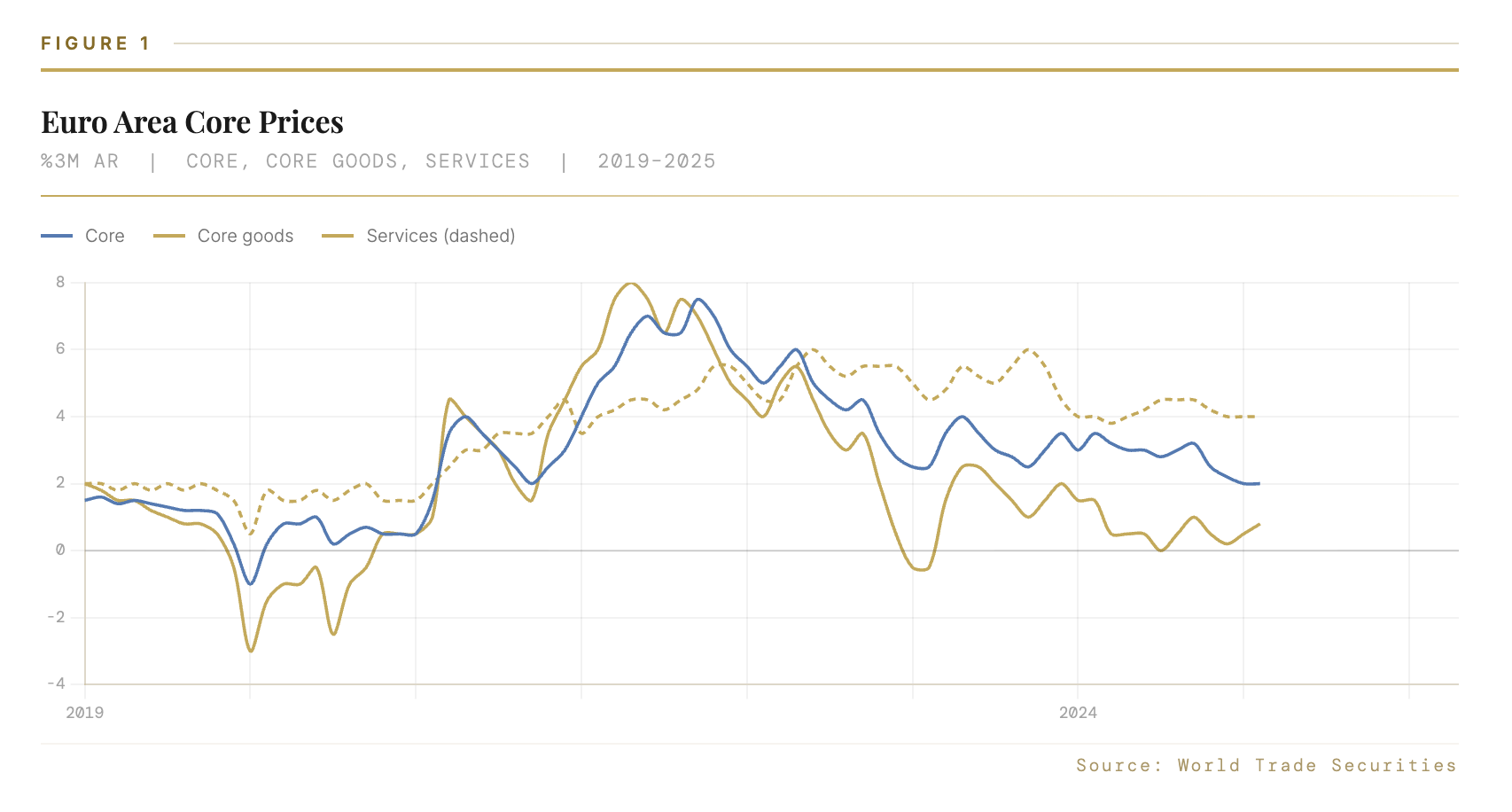

Progress on Euro area disinflation is undeniable. Headline inflation is now below 2%oya having peaked at 10.6% two years ago. Meanwhile, core inflation is now 2.7%oya, a 3%-pts drop since March 2023. The latest core price data are encouraging as services inflation, the sticky part of core, is showing signs of less high-frequency momentum. Earlier stickiness in services inflation appears increasingly linked to a relatively narrow set of categories, including insurance, health, administered prices and rents. In our view, their contribution to services inflation should decline over time.

The broader picture is also compelling. The GDP deflator and survey-based indicators are hinting at weaker pricing power. Wage inflation, in our view, should also decline next year and modest productivity gains should should offset some of the labor cost pressure. We thus take comfort from recent developments as we expect core inflation to decline further in the coming quarters and reach 2% by late 2025, a bit earlier than the ECB staff projection.

Recent progress is where it matters

Core inflation declined significantly in recent quarters. This decline, however, has been skewed to core goods, down 6.4%-pts from its early 2023 peak to 0.4%oya last month. Meanwhile, services price inflation only declined 1.6%-pts to 4.0%oya and has been stuck there over the past year. The latest data, however, are encouraging and suggest that services inflation has been less sticky of late (Figure 1). Averaging over the Paris Olympics period, services were running at a 3% ar over August-September, while those gains were closer to 5% ar in the early months of the year. In the core goods basket, price pressure remains weak (0.8% ar over the last 3 months), leaving core price gains as a whole close to 2% ar over the last two months.

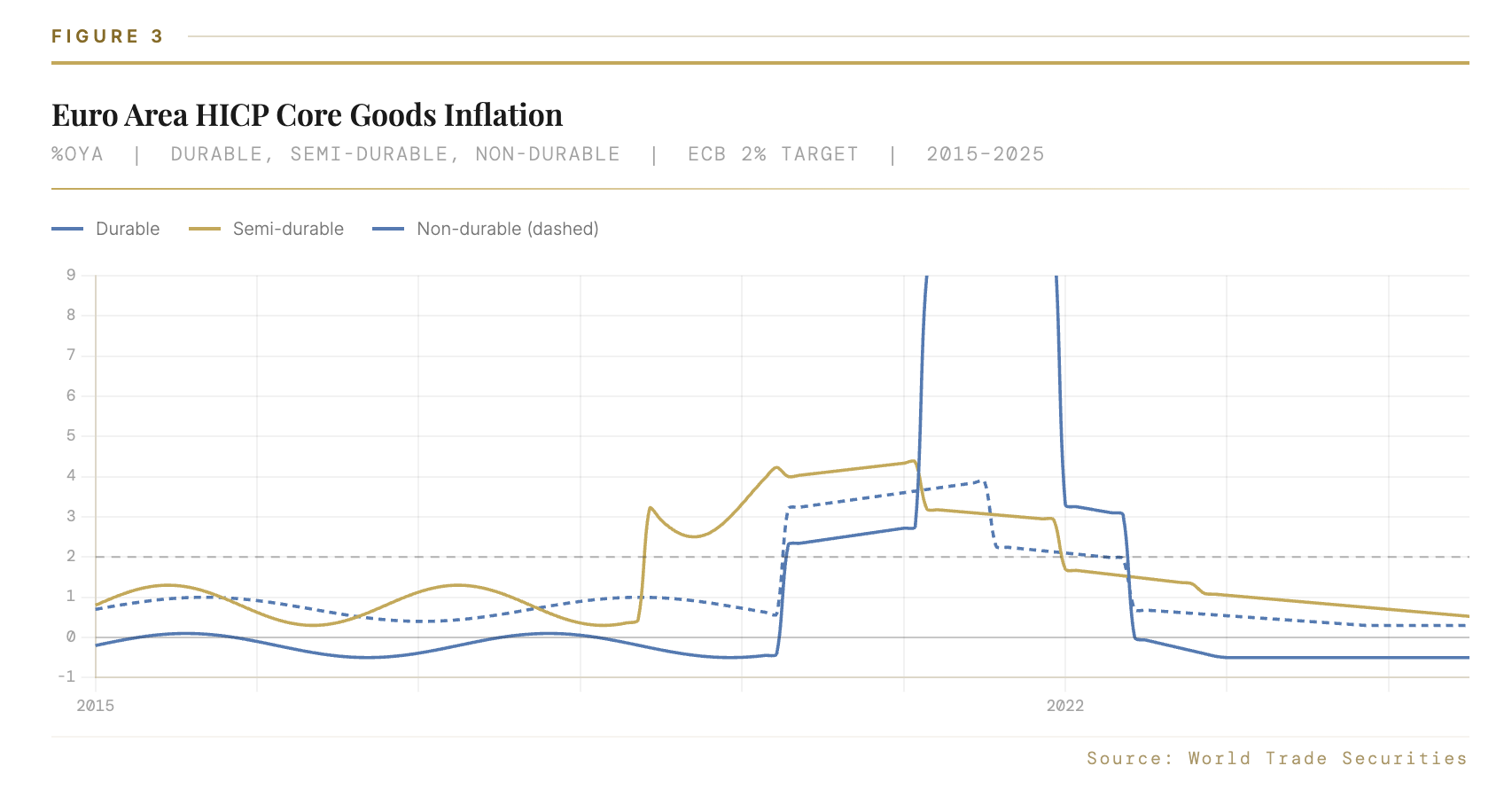

Core goods mostly back to normal

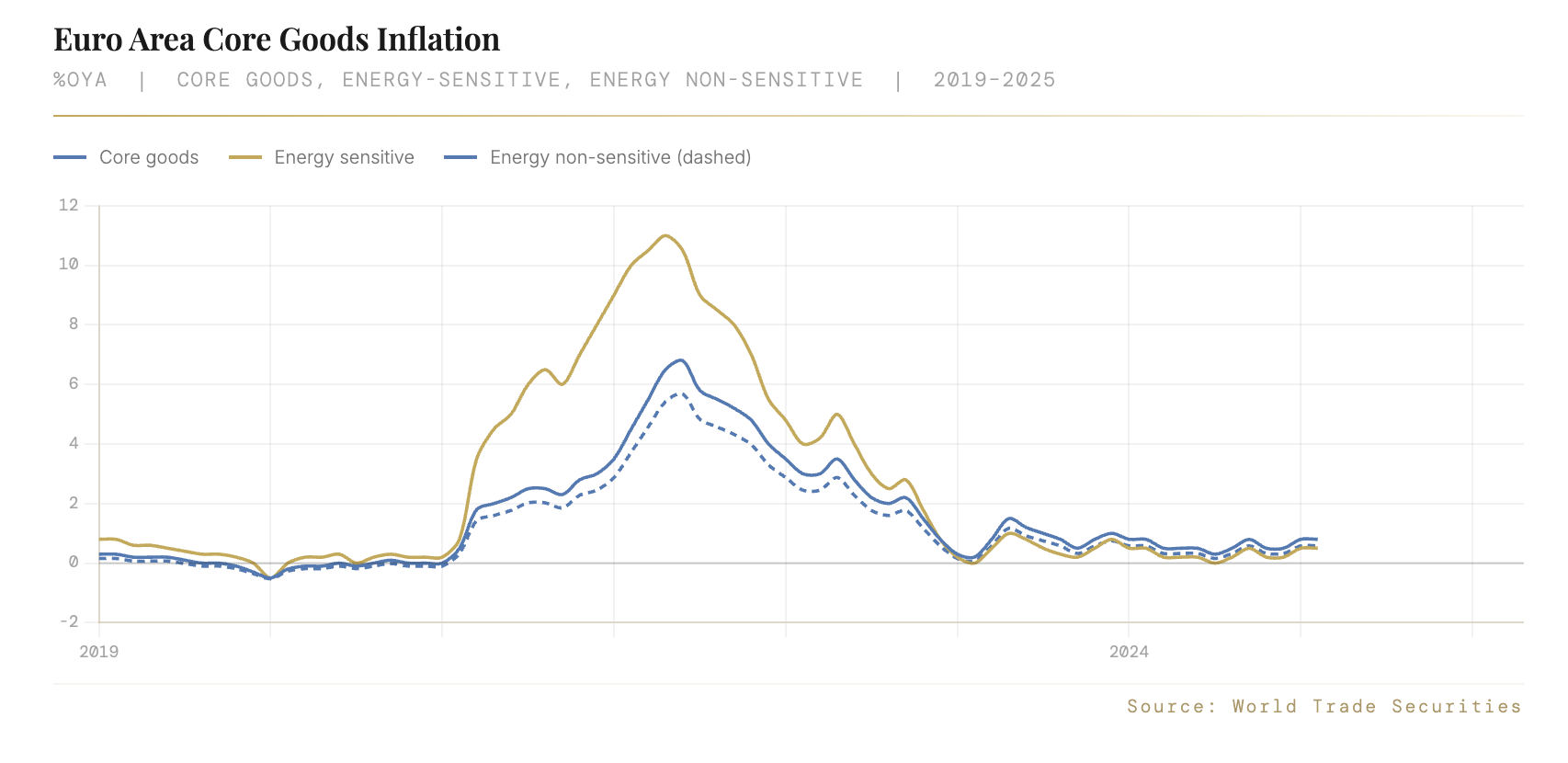

Core goods price inflation has declined sharply in recent quarters. This decline is largely owing to the fading of gas and electricity prices (Figure 2). High gas and electricity prices lifted core goods price inflation significantly in 2022, impacting energy-sensitive items. With gas and electricity prices now at much lower levels, this source of pressure has now faded.

The decline in inflation looks broad based in the core goods basket. Semi-durable and non-durable goods inflation nonetheless remains above pre-COVID levels.

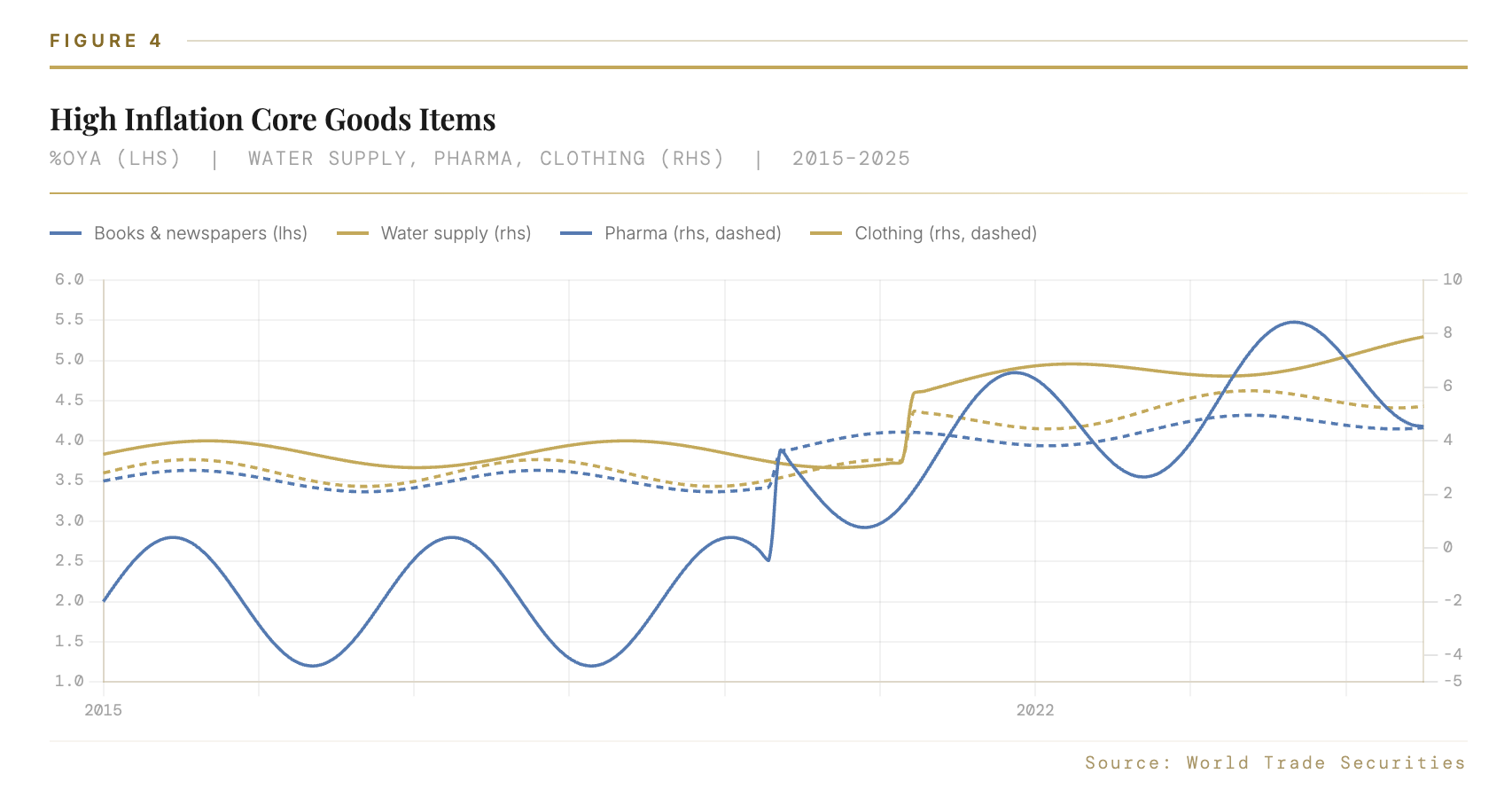

This outcome is due to a few items, which can be grouped into three categories (Figure 4). First, books and newspapers are part of the paper industry, which is energy intensive. Thus, some decline in their inflation rates looks likely going forward given the declines in gas and electricity market prices. Second, clothing and footwear price inflation remains high. While goods demand overall has been weak, clothing industries seem to have retained some pricing power. Finally, water supply and pharmaceutical products are impacted by administered prices, which likely have been driven by some lagged price-resetting mechanisms. In our view, there are reasons to think that price pressure linked to these factors (in particular energy driven and administered prices) may fade over time.

Remaining pressure points in services

While core goods price inflation has returned to normal, services prices have been stickier. But recent data do show some slowing. Through the noise associated with the Paris Olympics, services prices have been running at a 3% ar pace of late, less than the 3.5% seen in the spring and the 5% ar pace seen in the early months of the year. In the details, however, inflation remains high across a number of categories:

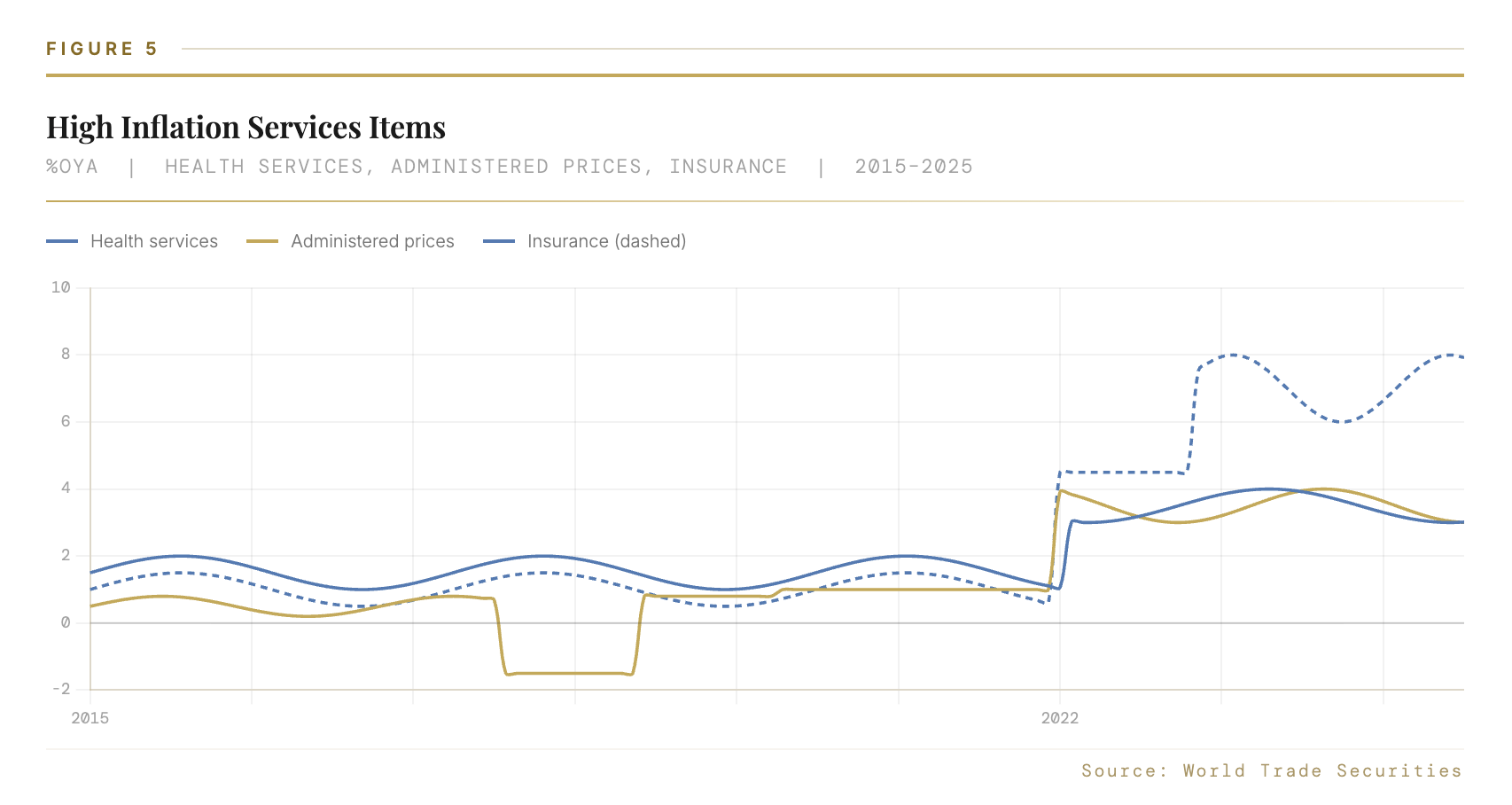

– Insurance inflation rose sharply through the early part of the year, but the inflation rate of these items has now stabilized. We interpret this outcome as a price resetting mechanism concentrated in the early part of the year, reflecting the high repair and replacement cost of insurance providers that they are now passing on as higher premia. The inflation rate in these categories lifted core inflation by 0.1%-pt this year (0.2%-pt for services inflation) and will stay in the numbers for the rest of the year. We assume a decline in inflation as we transition into 2025.

– Health inflation, meanwhile, increased significantly during 2023 and has plateaued in recent months. This pricing is, to some extent, linked to government decisions (e.g. hospital prices in the public sector) and a similar inflation pattern is observable for social protection. We assume that some of the cost pressure (inputs) has already faded and some fading is yet to come for costs (wage inflation), which should translate into a lower level of health inflation down the the line.

– Administered prices had an impact on services prices (and core goods prices as seen earlier). This includes postal, education, refuse and sewage prices. Price resetting was likely at play, based on higher costs, but the inflation rate of these items has plateaued in recent months, which is encouraging. The need for fiscal consolidation in some countries, however, may put pressure on such prices going forward.

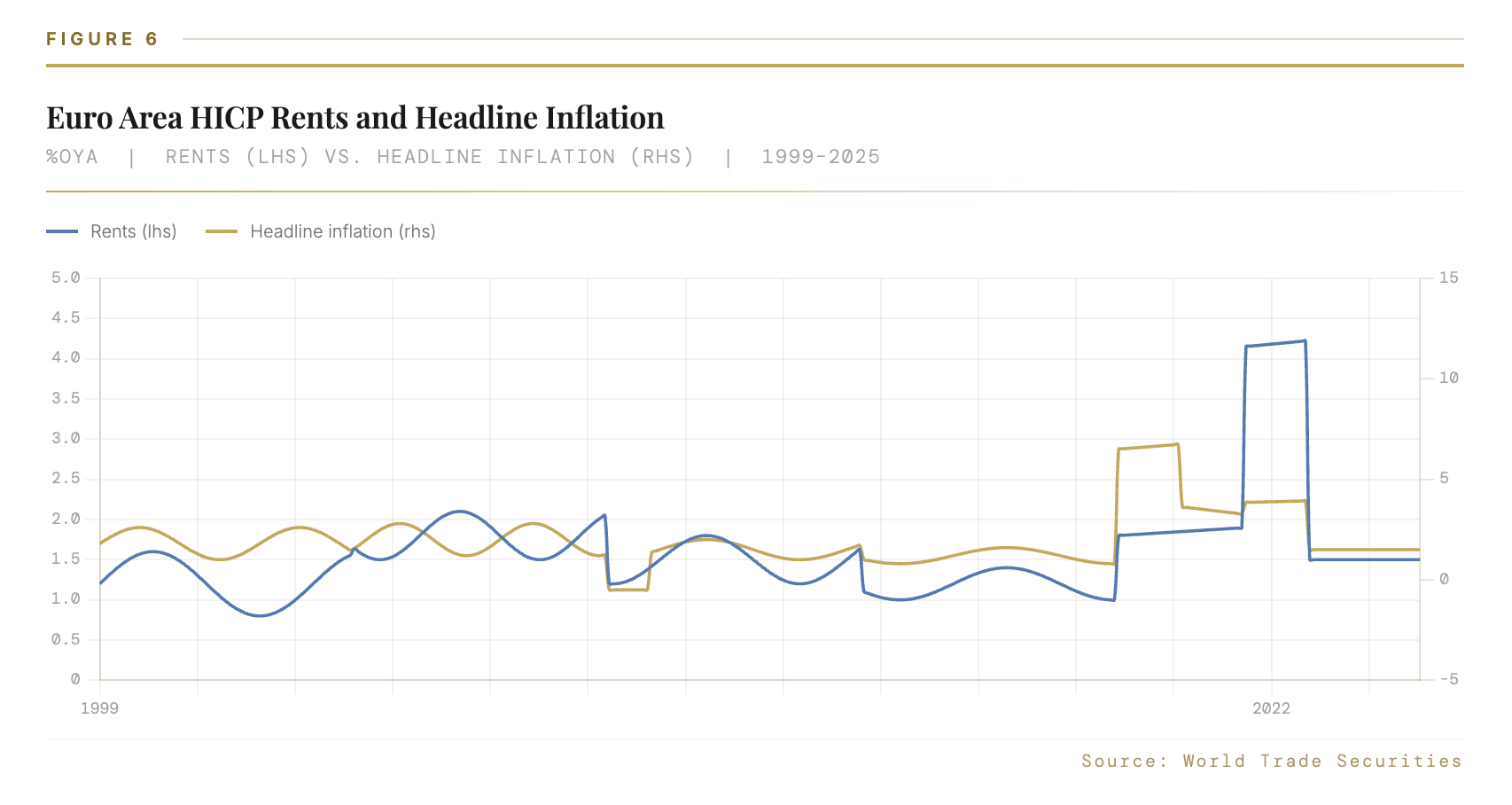

– Rents have been an important driver behind the stickiness in services price inflation. But there are reasons to think that rents inflation could come down. We found some (loose) empirical relationship between rents and inflation (rents in some countries are indexed to inflation), thus the lower level of inflation may have some impacts on rents. Also, house prices are down (rents could be seen as a return on investment) and mortgage rates have started to decline (a cost that home owners may have passed to tenants), suggesting rents inflation may soften in the coming months.

The future looks brighter

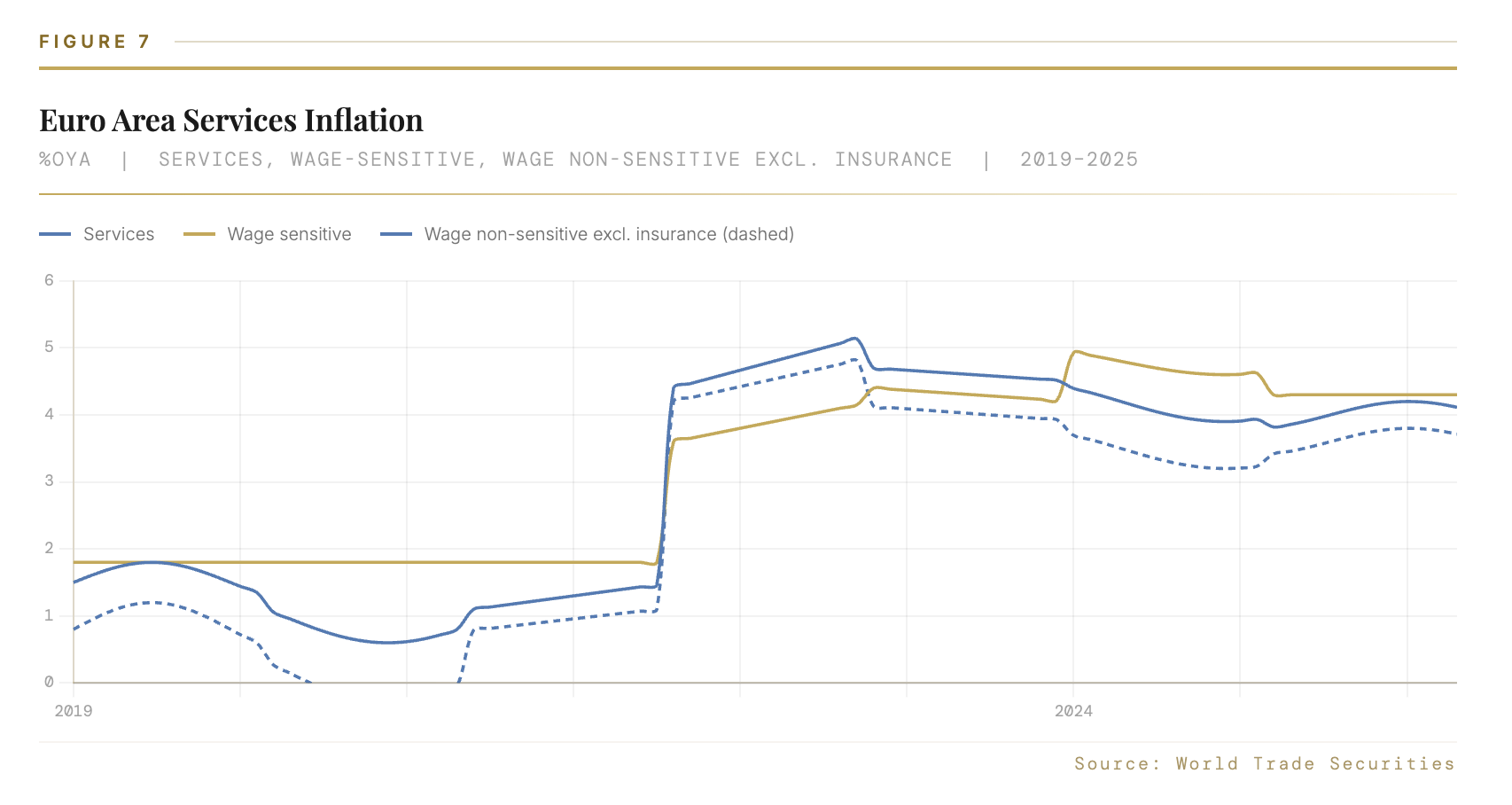

According to the ECB, 35% of the services basket is wage intensive, thus wage inflation is an important driver for services inflation. Using the ECB decomposition, we find that wage-sensitive services inflation has been stickier than the rest of the services basket in recent months. The inflation rate of wage-sensitive items came down from a peak of 5.2%oya in mid-2023 to 4.2%. Meanwhile, the decline in the rest of the services basket (ex. insurance) has been larger, from 5.6%oya to 3.6%oya.

We expect services inflation to decline in the coming quarters. Our modeling suggests that the rise in wage inflation in recent quarters has largely been driven by consumer price inflation: workers claimed for higher wages as consumer prices increased sharply . The impact of tighter labor markets in contrast was modest and productivity was weak in recent quarters. As the lower level of inflation gets embedded in wages negotiations, wage inflation in our view should soften.

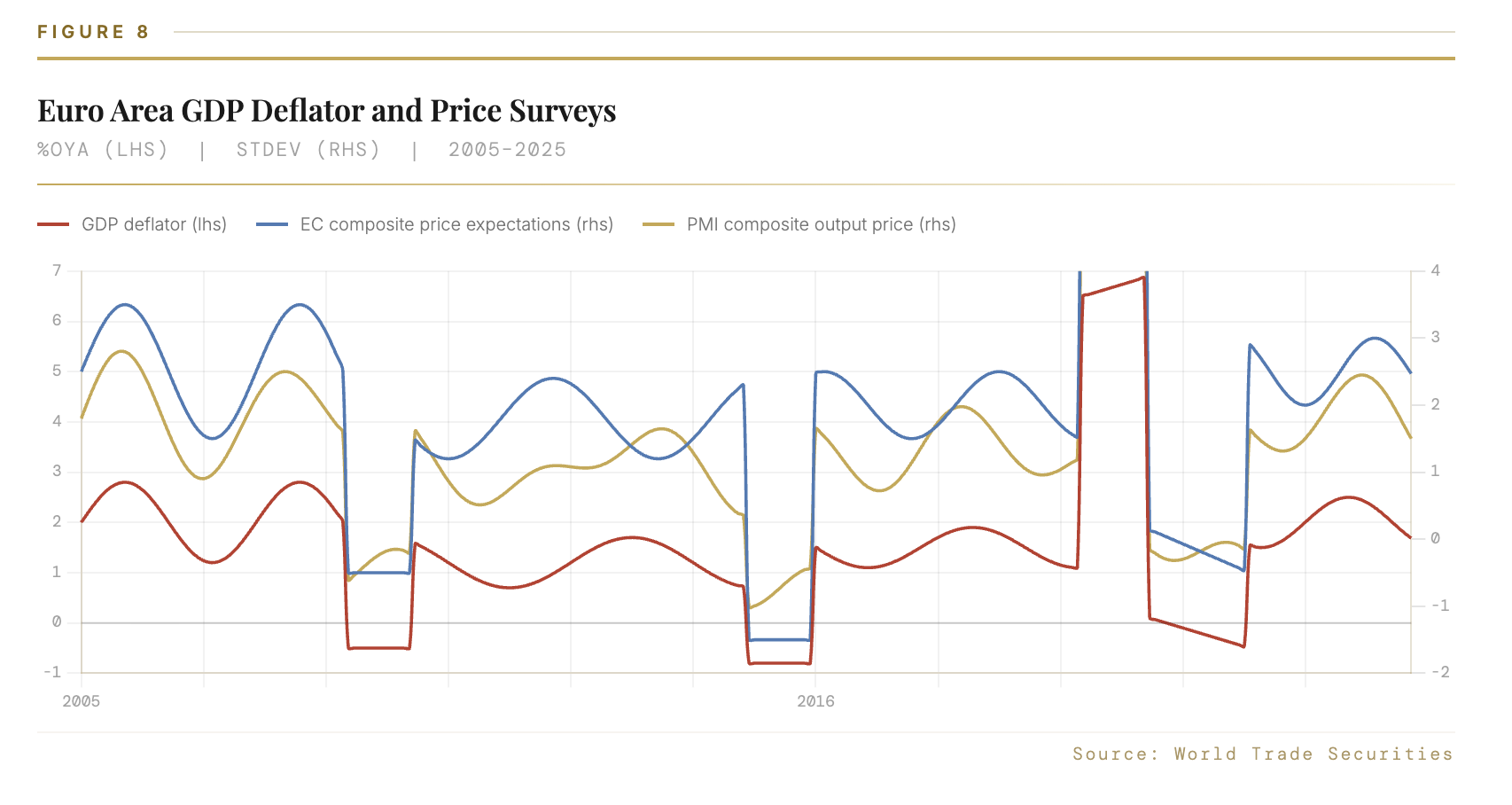

We also take comfort from recent deflator and survey data. The GDP deflator, a measure of domestic inflation declined sharply through 2Q (to 3.0%oya from a peak of 6.2%). With wage inflation still strong and productivity still weak, unit labor cost growth remains elevated at 4.6%, but the 2%-pt decline in recent quarters is encouraging. The shift in unit profit growth, now at -0.6%oya, meanwhile, suggests that corporate pricing power has faded significantly in recent quarters. The signal from surveys is furthermore suggesting that the GDP deflator should move closer to 2%oya in the coming quarters.

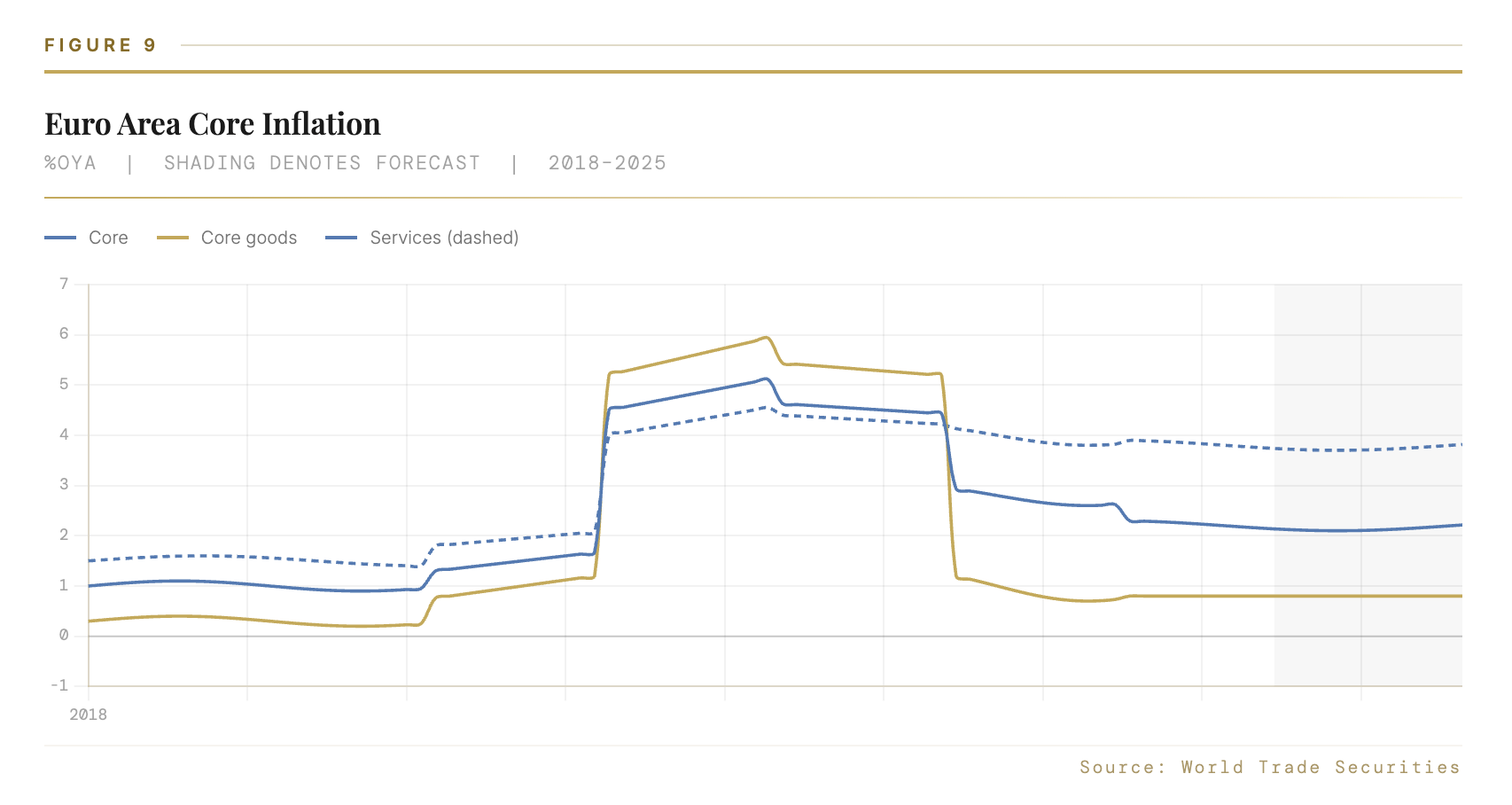

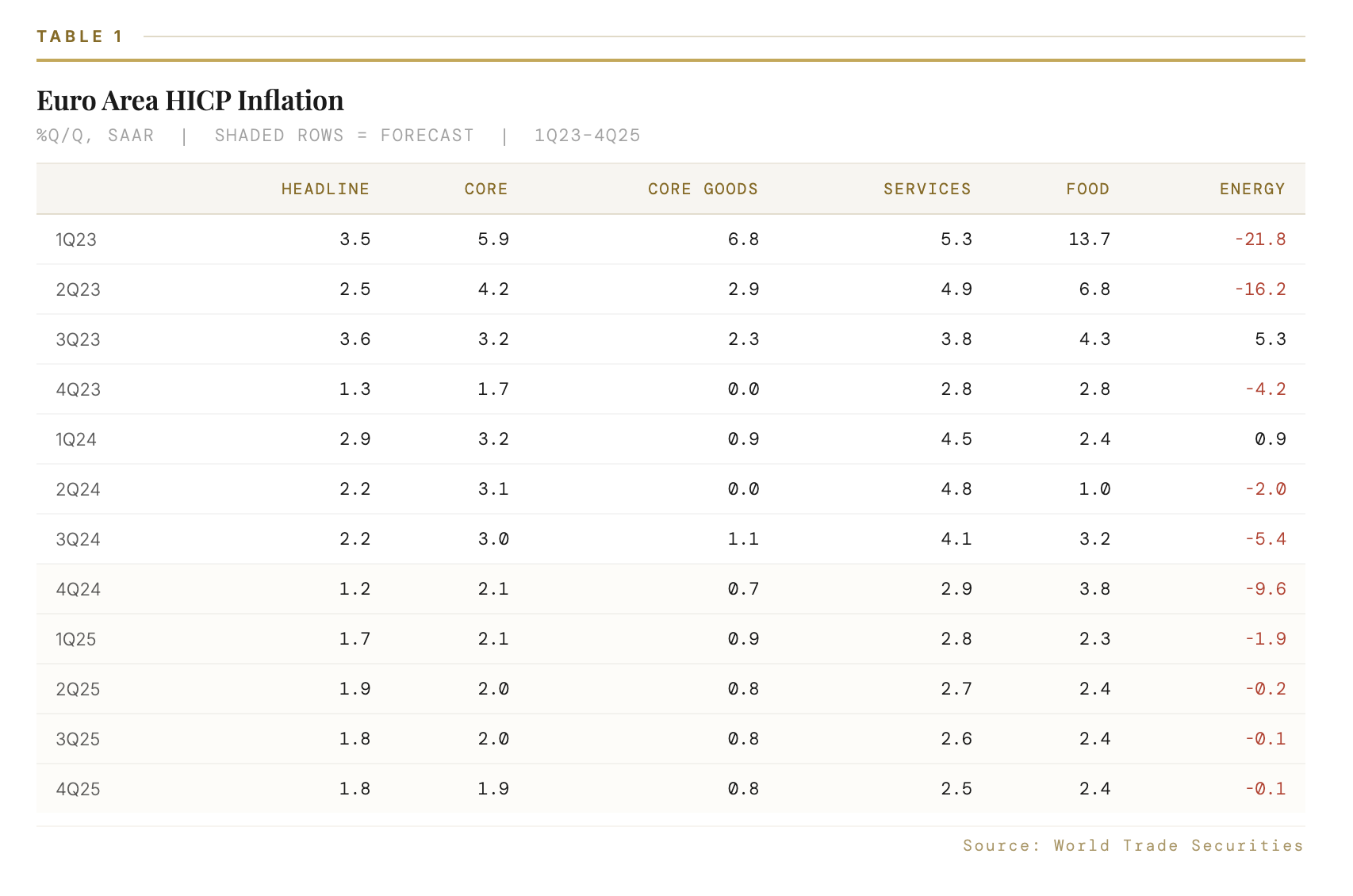

The recent data overall are a step in the right direction. We continue to expect core inflation to decline in the coming quarters, a decline driven by services. Core inflation in our forecast reaches 2% in 4Q25 (Figure 9 and Table 1). This is close to the ECB forecast, which sees core inflation reaching 2.1%oya in 4Q25.