- Sizable 2025 Ukraine support is already available, but concerns about military aid shortfall without US

- Only a gradual increase in national defense spending likely feasible and consistent with new fiscal rules

- Strong case for a centralized EU defense fund; German election is a key event

- Ukraine’s reconstruction unlikely to have near-term EU growth impact

The implications of Trump 2.0 for Ukraine and European defense spending are being widely debated. 2025 financial support for Ukraine looks to largely be in place based on existing agreements. An important question, however, is how to scale up European defense production quickly enough to offset a potential shortfall in US military aid in 2025. If production is not sufficient, the military equipment would likely have to be bought from elsewhere, including the US.

More generally, defence spending will likely have to increase further in Europe, perhaps to 3% of GDP according to NATO’s latest assessment of needs. This would be about 1% of GDP above current EU NATO member spending. If achieved over 4 years, that would imply extra non-defense fiscal consolidation of 0.25% of GDP in addition to around 0.4% of GDP per year likely required to abide by the new EU fiscal rules. Adjustment needs would be particularly high in France, Italy and Spain (greater than 0.75% of GDP per year). A European joint defense fund of around EUR500bn—potentially including the UK and Norway—would make sense from an efficiency and scale perspective, while possibly alleviating near-term national fiscal consolidation pressures depending on the design and financing.

As of end-23, Ukraine reconstruction was estimated to cost $0.5 trillion and be a decade-long project. With war still raging and most of the reconstruction financing still to be identified, we don’t think a near-term boost to EU growth is likely.

More focus on peace deal under Trump 2.0

President elect Trump is pushing for a quick agreement between Russia and Ukraine to end the war. And while Ukraine has signaled resolute willingness in that regard, including to discuss territorial concessions, the Russian position does not appear to have shifted meaningfully for now from the pre-war set of goals. Of course, Russia might shift but our impression is that it will be hard for Russia to accept strong security guarantees for Ukraine. Indeed, a key complication is that Russia’s main demand appears to remain Ukraine’s political subordination, while the main objective of Ukraine (and its allies) is ensuring its security. So, a lasting agreement may take time.

Significant non-US donor support for 2025

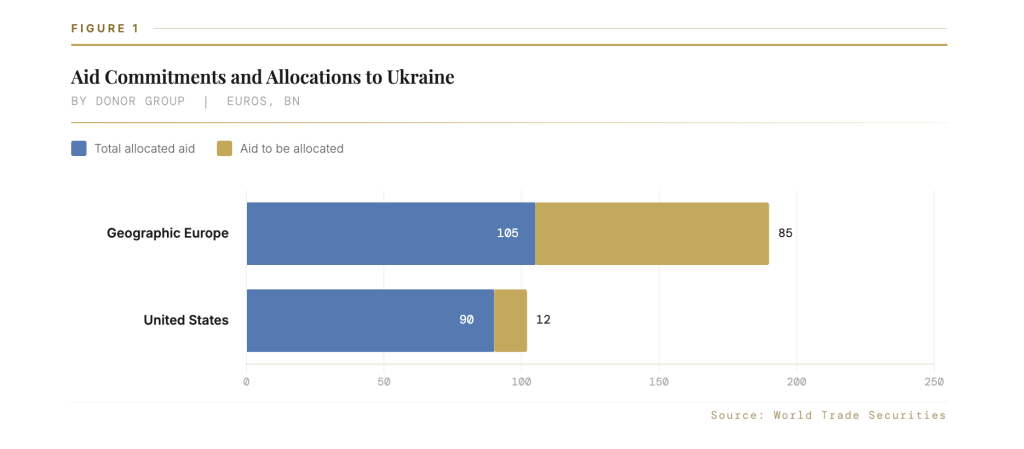

Given the large imbalance versus Russia, Ukraine’s economic and military resistance is underpinned by donor support. The Kiel Institute tracks this support, with Europe as the largest supporter in nominal amounts and in terms of GDP

(Figure 1). From early 2022 to August 2024, Europe had allocated EUR118bn, and the US EUR85bn. Commitments are higher (EUR 192.3bn for Europe). This suggests room to allocate more funds, including based on the “Ukraine Facility” (a 2024-2027 EUR50bn package).

All of this is even before taking account of the G7 Extraordinary Revenue acceleration (ERA) initiative. ERA provides $50bn of loans to Ukraine to be disbursed from December 2024-27. The EU is contributing EUR18 billion, with the UK and Japan providing another $5bn each. The US has disbursed $20bn.

Overall, on the financial side, there are significant non-US funds in the pipeline. US financial support was already in decline (to about US$9bn this year outside of ERA from about US$17bn in 2022) as Europe stepped up. Thus, even if US financial support were to be fully cut under Trump 2.0, other allies should be able to compensate for it.

Replacing US military aid quickly is hard

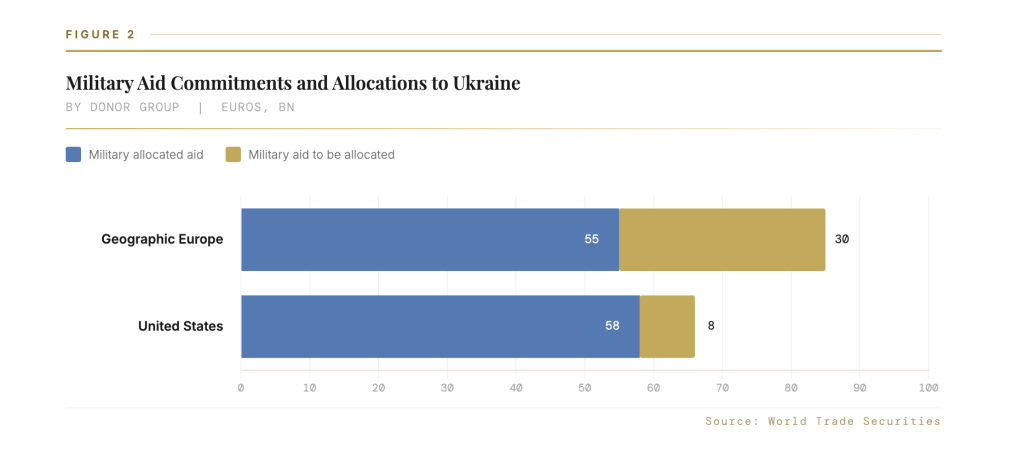

A key question remains: can Europe replace military aid from the US if it dries up under Trump 2.0? Nato did commit in July 2024 to provide a minimum baseline of EUR40 billion of military aid in 2025. But details are lacking. Up until now, military aid has mostly come from the US (EUR 56.8 billion), although Europe has been catching up when you add the contributions of the UK and other Nordic countries to those of EU countries (Germany being the biggest contributor in the EU—Figure 2).

According to Kiel institute estimates, without new US military aid packages, there could be a hole of about EUR25 billion in 2025 to fill. This is not a large amount (about 0.125% of EU GDP) and could anyway be on the high side given some aid has been advanced and with a further acceleration likely in the final weeks of the Biden administration. But, politically it would be challenging to create room for extra military spending in Europe given other spending priorities and the need for some of the largest European countries to reduce debt ratios. This has been demonstrated in the debate over 2025 German Budget, which amongst other things has precipitated early federal elections in February 2025.

Moreover, it’s not just about military funding but also the ability to scale up domestic military equipment production quickly. As noted in a recent Bruegel piece, European defense spending has increased substantially in the last few years but only after many years of underinvestment. Thus, it will take time for production to be ramped up and for military equipment stocks to increase. For example, a Kiel institute report estimates that at current procurement rates, Germany would take 15 years to re-establish 2004 capabilities in combat air- craft, whereas Russia could produce the equivalent of the Bundeswehr’s entire arsenal in 6 months.

Overall, it is hard to see how Europe can provide sufficient military equipment to offset a large US shortfall in 2025. Indeed, President Zelensky recently stated that Ukraine will continue to fight if US cuts all support, but he does not see how Ukraine can win the war in that situation. One solution could be for European countries to purchase equipment from US defense contractors and channel it to Ukraine.

Can EU defense spending be ramped up?

War on the doorstep of Europe has been a wake up call regarding the need to increase defence spending. There was a long decline once the peak of Cold War tensions were passed, but defense spending started to turn upwards during Trump 1.0 and has increased further since the war in Ukraine. For EU NATO members in aggregate, defense spending is expected to exceed the 2014 NATO benchmark of 2 percent of GDP in 2024.

Of course, this masks wide cross-country heterogeneity, with countries such as Belgium, Italy, Spain, Portugal expected to be significantly below 2 percent of GDP in 2024, while Poland and the Baltic states—where the Russian threat is physically closer will be way above.

But as many experts have observed, 2% of GDP was established as a minimum threshold, and certainly may not suffice for today’s security challenges after years of underinvestment in Europe. Indeed, the chair of NATO’s military committee has suggested that 3% of GDP may need to be spent by NATO countries to implement the alliance’s defence plans.

How can European countries increase defense spending at the same time that many need to reduce debt to GDP ratios? The new EU fiscal rules do allow some wiggle room for increases in defence spending. For example, defense investments can be used as a “relevant factor” that the Commission and Council take into account before deciding steps under an excessive deficit procedure.

If defence spending has to be raised to 3% of GDP, this would be about 1% of GDP above 2024 EU NATO member spending. Current estimates suggest EU countries overall will have to structurally consolidate around 0.4% of GDP per year to abide by the new EU fiscal rules (the rules have debt declining with high probability once adjustment periods of 4 or 7 years are completed). So an additional defense spending build up gradually over 4 years would imply non-defense consolidation of around 0.65% of GDP per year. This is significant, but achievable, especially if a longer time horizon than 4 years were to be used. It would require very tough decisions, however, given age-related spending pressures and investment needs related to the digital and green transitions.