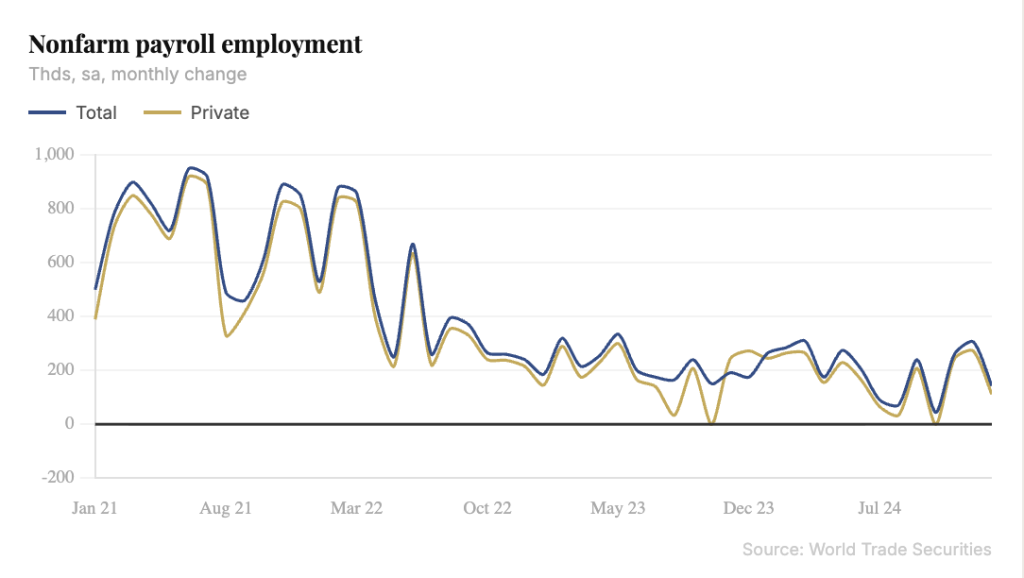

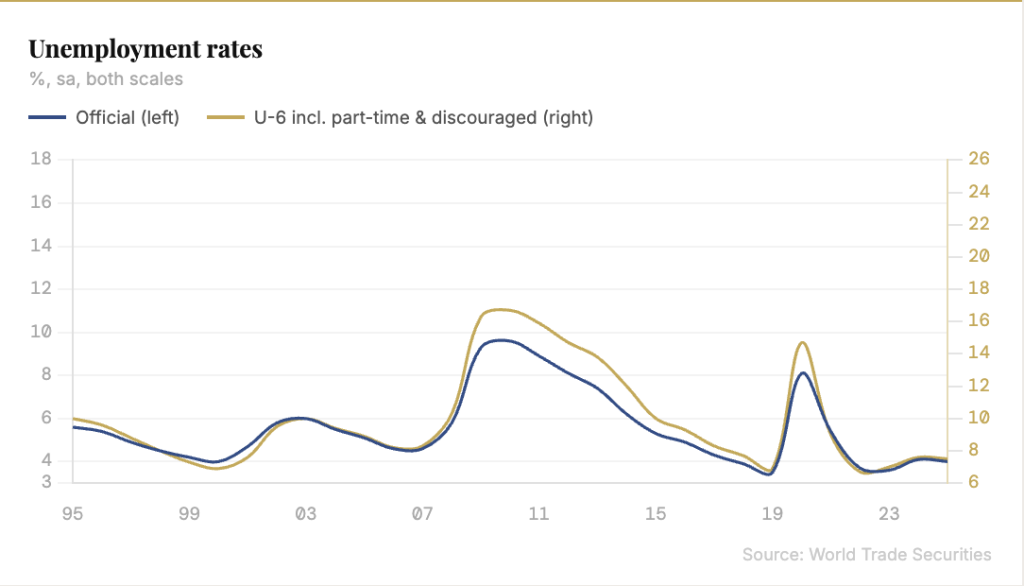

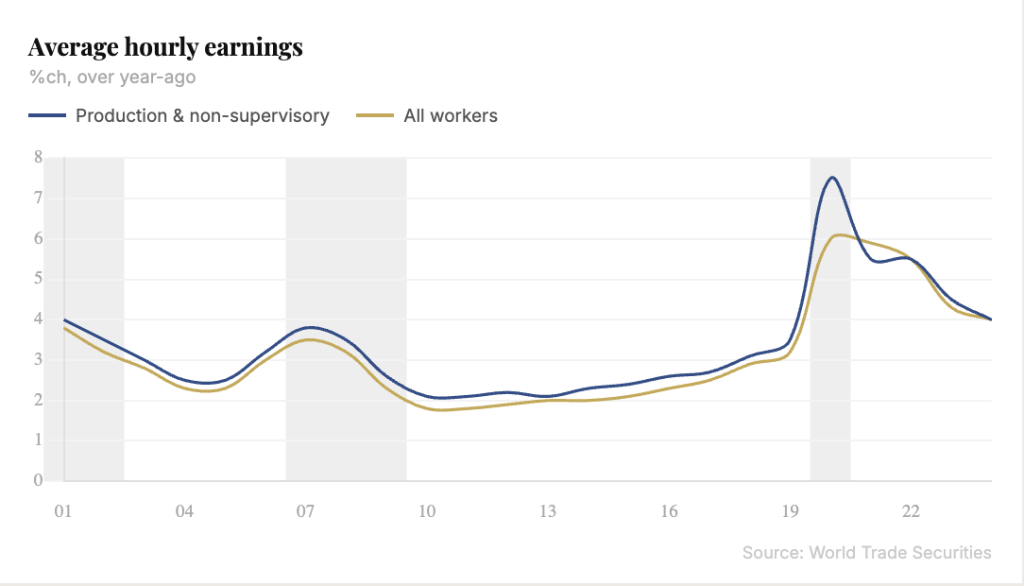

The January employment report was a little messier than usual, but the underlying message appears to be that the labor market looks just fine. Nonfarm employment increased by 143,000 last month, a smidgeon below expectations but, big picture, reasonably close to the revised 166,000 average monthly gain seen in 2024. The unemployment rate slipped a tenth to a 4.0%, the lowest level since last May. (As we discuss below, the unemployment rate tightened two tenths between December and January, after accounting for new population estimates). There were offsetting surprises to the upside on average hourly earnings, which increased 0.5%, and to the downside on the average workweek, which fell another tenth to 34.1 hours. These two surprises likely had one cause: unusually bad weather during the survey week, which lowered average hours worked that week, thereby boosting average hourly earnings for salaried workers. This shouldn’t distort the report’s estimate of nominal labor income, which on average over the past three months is growing close to 5% annualized; even with inflation still running up in the 2s, this is enough to support solid growth in real consumer purchasing power. For the Fed, what’s not to like? There are a lot of risks swirling around out there, but the hard data are coming in close to their Congressionally mandated goals. With an economy that ain’t broke there’s nothing to fix, and so the FOMC will likely be doing nothing for the foreseeable future.

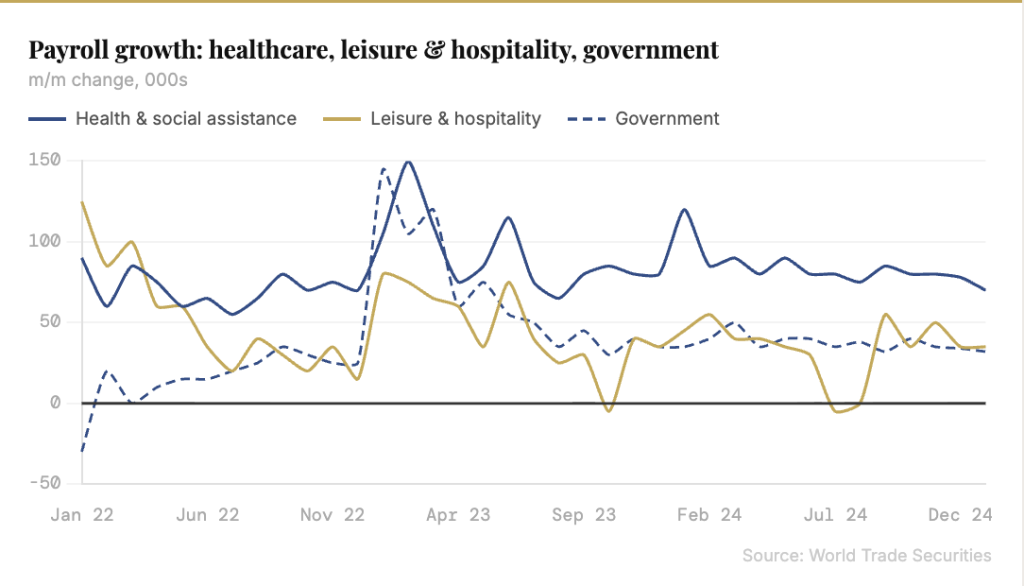

The establishment survey was published with the annual revision, which took down the level of employment last March by 589,000 and in December by 610,000; this was close to what had previously been signaled by BLS. In the monthly figures, that downward revision is estimated to have occurred in the first three quarters of last year; gains in Oct-Dec were all revised up somewhat. Turning to January’s 143,000 gain, there were some now-familiar patterns in the data. Government employment was up 32,000; health case and social assistance employment was up 66,000 and accounted for more than half of the 111,000 increase in private employment. Leisure and hospitality employment slipped 3,000, which may reflect a weather effect. The increase in average hourly earnings left the year-ago gain unchanged at 4.1%. The average workweek last month was the lowest since early 2010 (excepting March 2020), with the unrounded figure slipping 0.17 hours. Earnings for production and non-supervisory workers also increased 0.5% last month (4.2% over year-ago) and the average workweek fell 0.2 hour to 33.5 hours. Most industries saw an acceleration in earnings growth and a decline in the workweek, which is consistent with a weather story, but a more conclusive verdict will have to await the regional data released in three weeks.

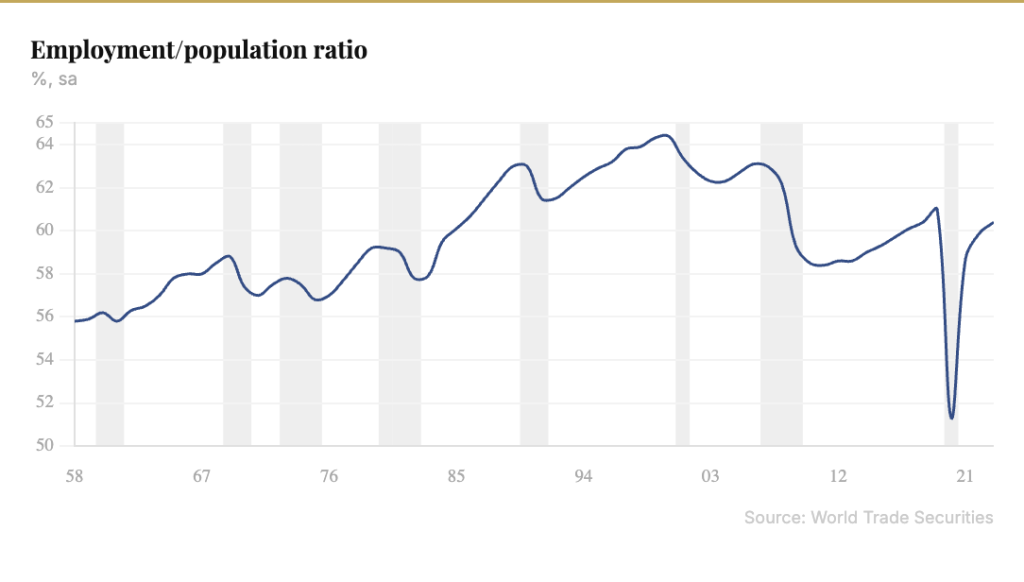

Turning to the household survey, the annual adjustment to population estimates complicated the message coming from this survey, though it’s safe to say the message is a favorable one. Due in part to updated international migration estimates, the over 16 population estimate was raised by an unusually large 2.9 million. This in turn boosted estimates of the labor force by 2.1 million and employment by 2.0 million. Household employment is now up 2.7 million over the last year, no longer trailing the establishment survey estimate of 2.0 million. BLS doesn’t revise prior months’ estimates in the household survey, but had these figures been in place earlier the December unemployment rate would have been 4.2%, and so the January number would have been a 0.2%-point decline. The updated figures would have also boosted the participation rate by a tenth, and so the December to January increase of 0.1pp to 62.6% was only due to new population estimates. Similarly, the employment-to-population ratio increased a tenth to 60.1% last month, but that was entirely a population estimate artefact. There were 591,000 employed last month but not at work due to bad weather, which is about double the median figure of 284,000 for Januarys over the prior decade.