The FOMC cut the funds rate today by 25bp to 4.0-4.25%. There was only one dovish dissent for a larger cut: 50bp from new governor Miran. Moreover, in the press conference Powell suggested 50bp wasn’t seriously entertained by the Committee. Unlike the last meeting, both Governors Bowman and Waller voted with the consensus this time. While this might take them out of the running to be the next chair, it does signal that the independence of the institution may be more durable than some have feared. The forward-looking news today was mixed. Both the dots and the statement were more dovish than we expected.

However, Chair Powell’s press conference was more hawkish. He downplayed the dots and characterized today’s move as a risk management cut, a characterization which casts doubt on whether today’s move is necessarily the start of a long easing cycle. Even so, we are comfortable in expecting another cut at the next meeting, as well as the two meetings after that. In our view, it would take a major reversal in the loss of momentum in labor market activity for the Fed not to ease next month. The post-meeting statement was revised dovishly, as it now notes that downside risks to employment have risen. Note that this discussion of employment risks was in the outlook discussion, meaning those risks have risen even after today’s rate adjustment. The description of incoming data was mixed. On the dovish side, the statement noted that “job gains have slowed, and the unemployment rate has edged up”. However, on the hawkish side it has now also noted that inflation has moved up. Even so, the discussion of downside employment risks is more meaningful for the outlook. As Powell summed up in the press conference, “It’s really the risks that we’re seeing to the labor market that were the focus of today’s decision.” Consistent with this, it was also observed in the press conference that the unemployment rate projections in the SEP (discussed more below) didn’t move up.

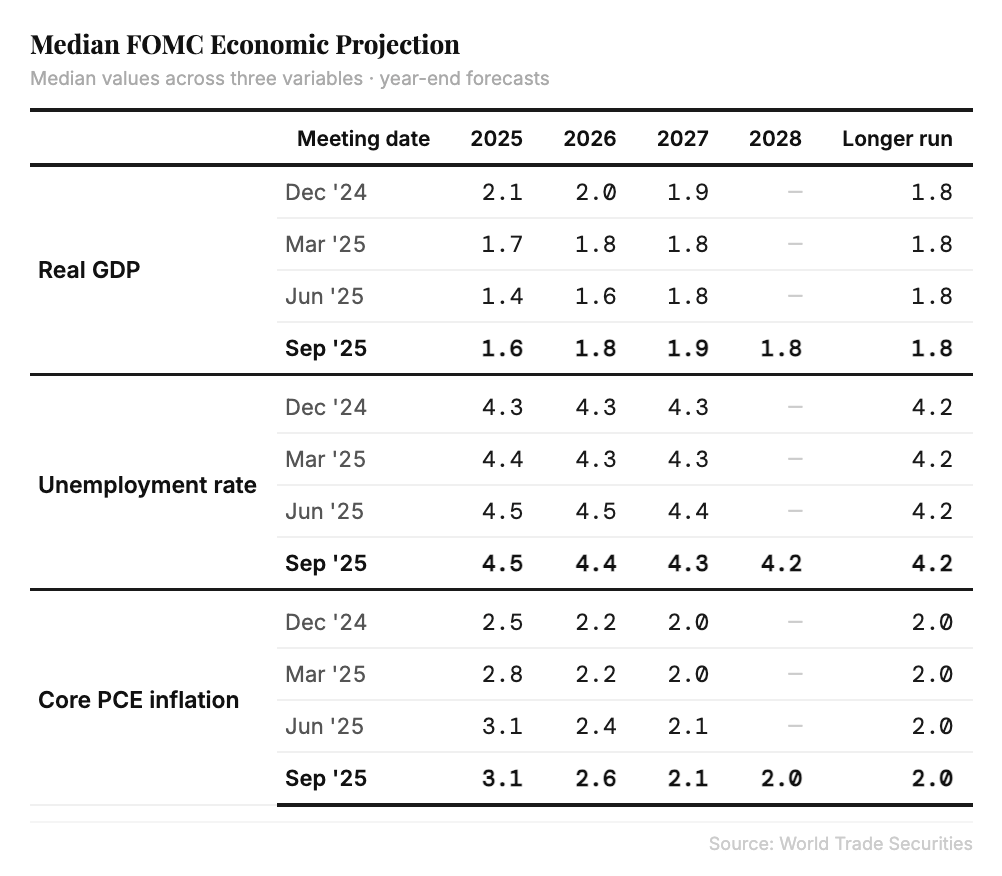

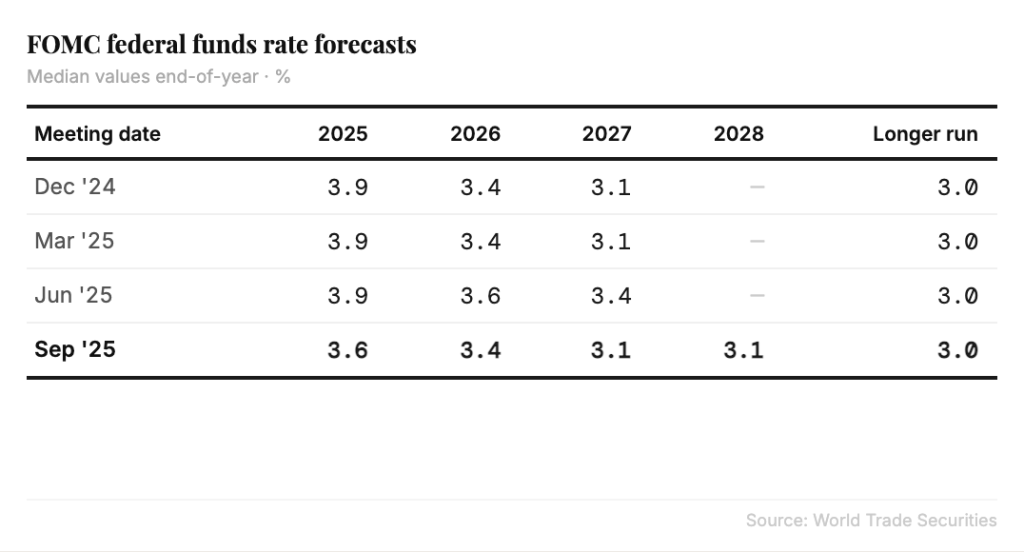

This all relates back to Powell’s characterization of today’s move as “a risk management cut.” Last year’s cuts were also risk management cuts, which opens the possibility that the current cycle could end after only a handful of cuts, provided employment risks aren’t realized. The median dot for this year surprised dovishly, indicating another two cuts. As alluded to earlier, Chair Powell downplayed the significance of this signal. Indeed, nine participants projected one or fewer cuts, nine projected two cuts, and one, Miran, looked for 150bps of cuts. As such, it’s possible that Miran’s replacement of Kugler was enough to tip the median from one to two. Beyond this year, the level of the median dot for the out years was in line with expectations: another cut in each of the next two years, which would bring rates to a new neutral of 3.125%, up an eighth from the June projections. There were only small changes to the economic outlook, none more than two-tenths in either direction. Growth was revised up a little higher in all three years relative to the June projections; this could reflect 3Q tracking as well as incorporating a larger OBBBA. Unemployment is revised down a tick in the next two years. Inflation was revised up two ticks next year. None of the longer-run projections changed, save for the neutral interest rate, which continued its slow march higher

At the press conference, Chair Powell noted that “there are no risk-free paths now. It’s not incredibly obvious what to do, so, we have to keep our eye on inflation. At the same time, we cannot ignore and must keep our eye on maximum employment.” While conceptually ambiguous, we expect that the Committee will prioritize the employment mandate for the remainder of the year, particularly as growing labor market slack should limit second-round inflation effects from tariffs.