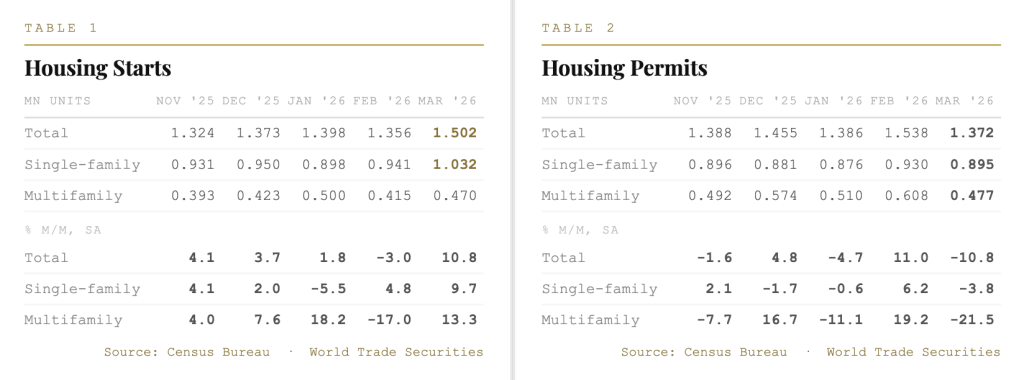

The combined February and March housing starts report delivered a strong rebound in the single-family segment following a weaker than initially reported start to the year. Downward revisions to January confirmed that severe winter weather weighed on construction activity to a greater degree than last month’s release suggested, but single-family starts recovered 4.8% month-on-month in February and surged a further 9.7% in March to reach 1.032 million saar. Total starts climbed to 1.502 million saar in March, the highest level since December 2024. The headline is unambiguously strong. The forward-looking data are less so.

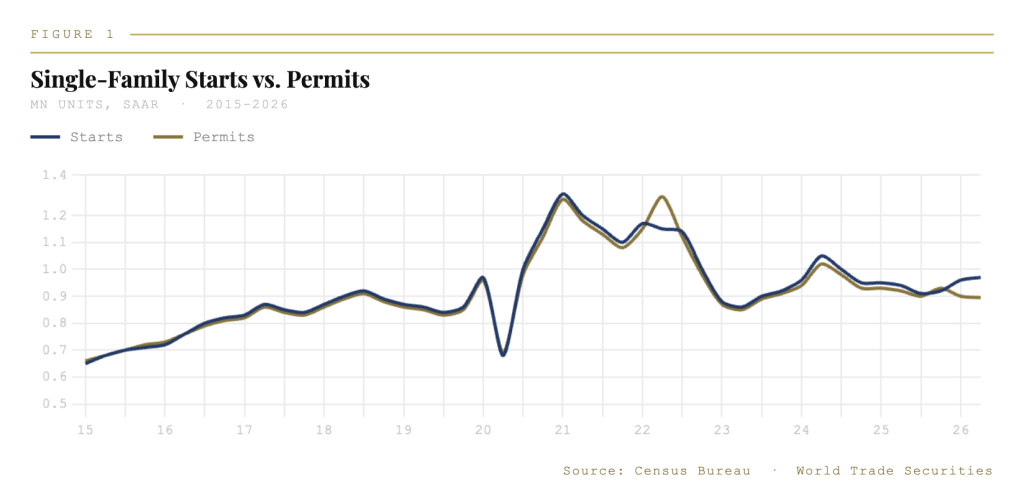

Building permits fell 10.8% month-on-month in March after a strong February, and single-family permits declined 3.8% to 895,000. The divergence between firmer starts and softer permits is the central tension in this release. Permits lead starts by several months, and their sustained softness over the year to date suggests that builders are executing on previously authorized projects while growing more cautious about future commitments. The NAHB homebuilder confidence index reinforces this reading, having slumped to a seven-month low of 34 in April, with the gauge of expected sales over the next six months falling seven points to its lowest reading since June. That deterioration in forward confidence is not consistent with the March starts headline, and history suggests it is the survey data, not the single-month print, that better anticipates near-term construction activity.

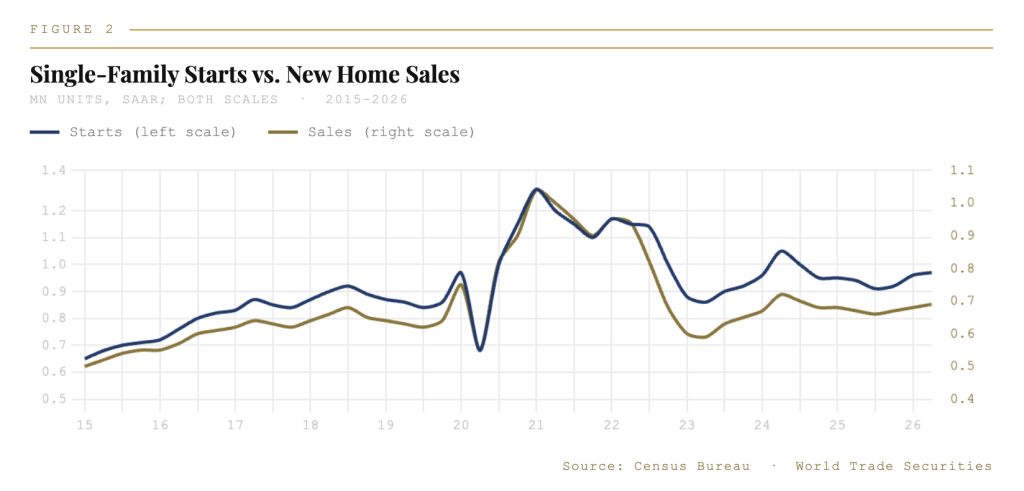

The broader demand picture remains mixed. New home sales plunged 17.6% month-on-month in January to a four-year low of 587,000. Months’ supply surged to 9.7 in January, and the inventory of completed single-family units reached a post-pandemic high. Builders facing that inventory overhang are likely to prioritize clearing existing stock before ramping new construction — a dynamic that will weigh on starts over the coming quarters regardless of permit authorization levels. Mortgage purchase applications have moved sideways since April, with rates remaining elevated relative to the start of the year, and higher energy costs from the Middle East conflict are beginning to feed into building material prices in a way that adds to per-unit construction costs.

On a year-to-date basis through March, single-family starts are down 5.8% relative to the same period last year. Permit issuance has trended lower since the start of the year. WTS continues to track a contraction of approximately 5.5–6.0% quarter-on-quarter saar in real residential investment for Q1 2026. The March starts rebound is real and welcome, but the weight of the forward indicators — permits, builder sentiment, sales, and mortgage applications — points to a construction sector that will remain constrained through the second half of the year. The structural housing deficit documented in last week’s household formation note ensures that any demand recovery will find insufficient supply to meet it. The shortage is not being addressed. The permits data say so.