On August 1, the US increased the reciprocal tariff on imports from Türkiye to 15%, up from 10%. Since March 2018, the US has imposed a 25% tariff on steel and aluminium imports from Türkiye,so that tariff is not new for the country, unlike the rest of the world. The US also announced a 25% tariff on autos and auto parts on April 2. Given that the US is Türki- ye’s second-largest export partner after Germany, Türkiye’s exports might appear vulnerable to US tariffs, however, our analysis demonstrates otherwise.

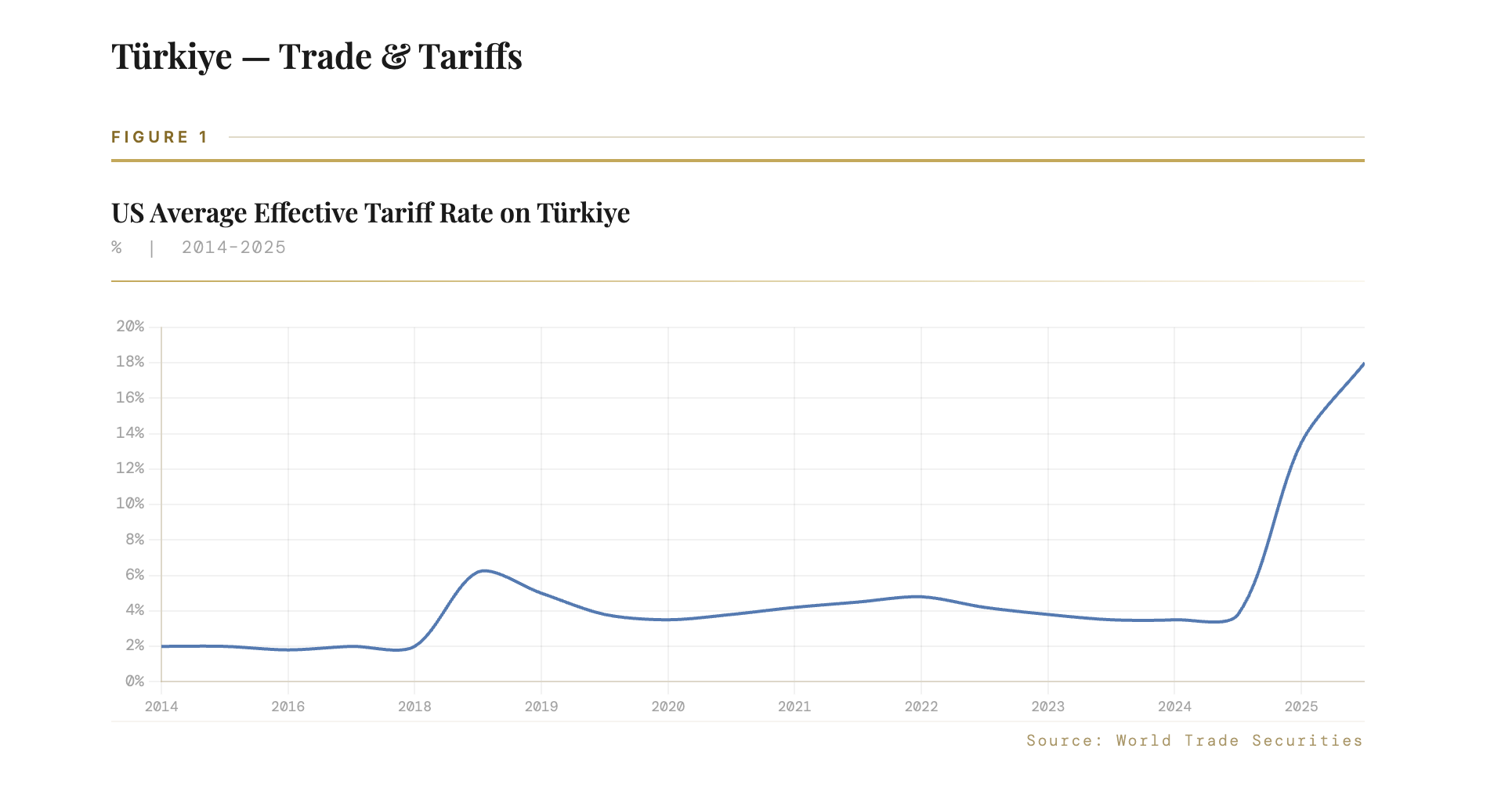

US tariffs on Türkiye Until March 2018, US tariffs on Turkish imports averaged a low 2.3%. In March 2018, the US imposed a 25% tariff on Turkish steel and aluminium, doubled it to 50% in August 2018 due to political tensions, and reduced it to 25% in May 2019. In April 2025, the US imposed a 25% tariff on autos & parts, then raised it to 50% in June. On August 1, the US increased the reciprocal tariff rate on Türkiye to 15%, pushing the average effective tariff rate to 18.1%.

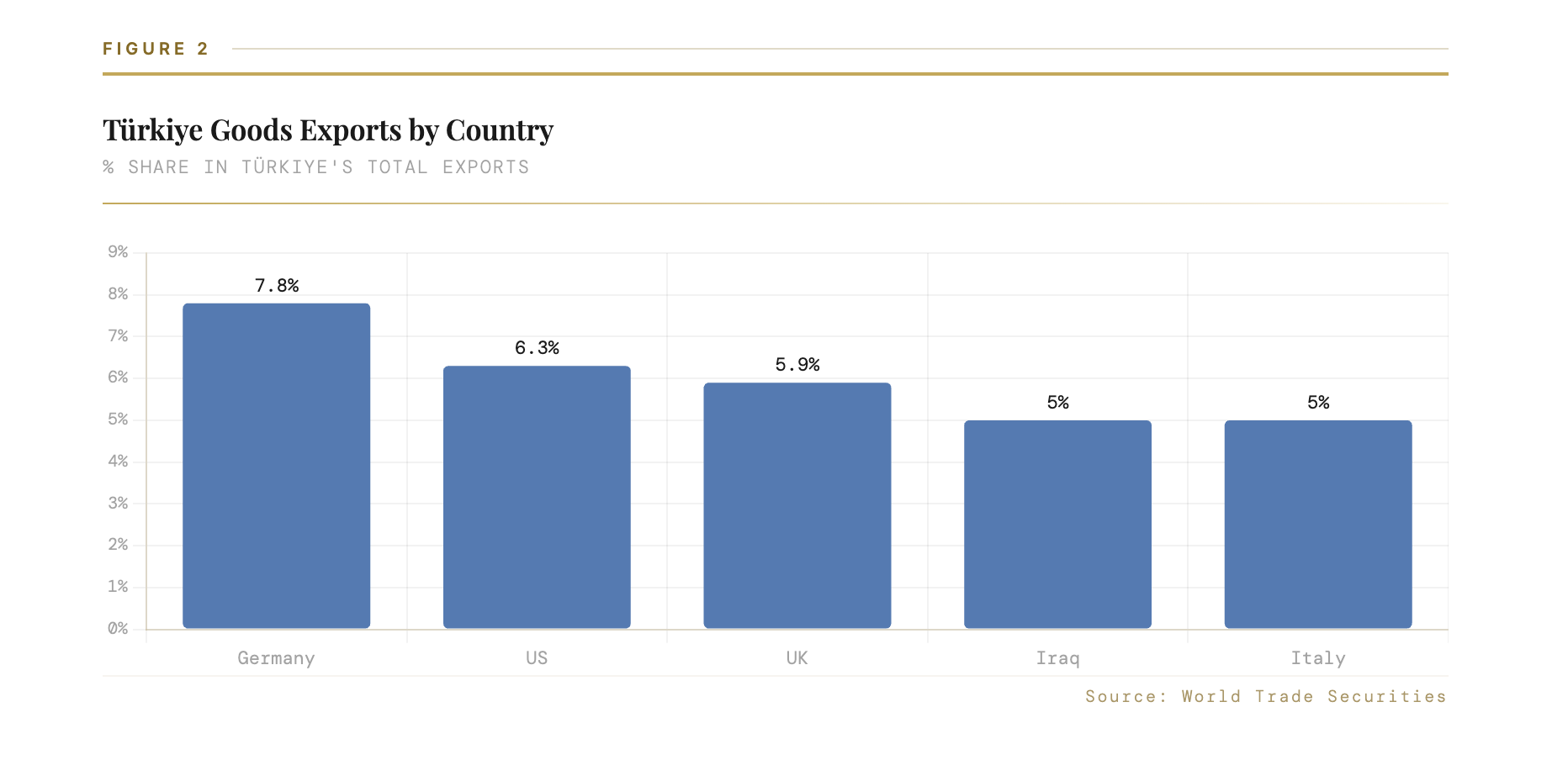

The US is Türkiye’s second-largest export partner after Germany, comprising 6.2% of Türkiye’s total exports. Türkiye’s exports to the US amounted to $16.4bn, or 1.2% of GDP as of 2024. As the Turkish economy is largely domestic demand-driven, the growth impact remains limited through trade exposure to the US tariffs.

Over the past decade, Türkiye’s exports to the US have accelerated, driven by robust performance in machinery and electrical equipment exports. However, the sectoral composition and recent trends in bilateral trade provide greater assurance regarding the limited impact of US tar- iffs. The goods trade between the US and Türkiye is balanced as of 2024, with Turkish exports to the US having declined since the pandemic, primarily driven by basic metals and autos & parts. The data reveals a significant structural shift in the composi- tion of Türkiye’s exports to the US post 2018. Tariffs on steel and aluminium, introduced from 2018 onwards, led to a pro- nounced decline in exports of basic metals as well as autos & parts.

The notable decline in the latter was attributed to the near-shoring of auto imports by the US, primarily to Mexico (Figure 4). Exports of aircraft parts also registered moderate declines, reflecting Türkiye’s removal from the F-35 programme in 2019 and the subsequent imposition of CAATSA sanctions in 2020. Given that a sharp contraction in auto & parts, iron & steel, and aircraft & parts had already materialised since 2018, the impact of new US tariffs imposed this year will likely remain limited (Table 1). US exposure is limited The trade statistics might obscure a deeper exposure—such as Türkiye’s potential indirect sensitivity to the US via the EU supply chain. But the data says otherwise.

The OECD’s trade- in-value-added database, which captures direct and indirect exports of embedded value added by country and industry, show this clearly. Focusing on the automotive, machinery, and electrical equipment sectors—the largest contributors to Türkiye’s exports to the US—Türkiye’s value-added embed- ded in final US demand amounts to only 0.05% of its GDP. This is significantly lower than its Emerging Europe peers, such as the Czech Republic, Hungary and Poland, whose trade exposure to the US ranges from 0.1% to 0.3% of GDP. Market sentiment channel Although the US is an important market for Turkish exports, the direct trade impact of the newly imposed US tariffs is expected to be limited. Should tariffs rise due to potential strains in

Türkiye-US relations, the impact would more likely be transmitted through the market sentiment channel rather than via trade flows. Instead, as observed during the August 2018 period, strains in US-Türkiye bilateral relations may lead to an increase in the country’s risk premium, resulting in higher funding costs.

Secondary tariffs unlikely In a surprising move, the US has increased its tariff rate on Indian imports to 50%, including a penalty of 25% for its sub- stantial imports of Russian crude oil. Market concerns have risen that other buyers of Russian oil, including Türkiye, could suffer similar action. Türkiye is the third-largest importer of Russian oil and natural gas after China and India. Russia supplied 66% of Türkiye s oil imports, and 41% of its natural gas imports as of 2024.

Türkiye has maintained a dialogue with the new US administration, however, the US has stepped up pressure on Türkiye to end imports of Russian oil and gas in September. As a ges- ture of goodwill, Türkiye terminated the retaliatory tariffs imposed in 2018 on US imports, which included products ranging from cars to fruits. Türkiye has also complied with the international restrictions, such as the G7 price cap on Rus- sian oil. For instance, Türkiyes largest refiner Tupras cut Russian oil imports in Jan-Feb 2025 after the price of Urals exceeded the G-7 price cap of $60 per barrel.

Türkiye`s private refineries, Tupras and Star, demonstrated their ability to source oil from alternative countries earlier this year (although these purchases were likely made at higher prices). Importantly, Türkiye primarily utilises oil and gas for domes- tic consumption rather than re-exporting, in contrast to India. Türkiye has also taken concrete steps to diversify its energy imports away from Russia. The state-owned gas company BOTAS signed a 20-year agreement to import 4bn cubic meters per year of US-produced LNG starting in 2026. In addition, Iraq resumed Kurdish oil exports to Türkiye last week following a 2.5 year suspension. Hence in our view, the risk of secondary tariffs for Türkiye remains low, thanks to improved bilateral relations with the US and Türkiye’s ongo- ing efforts to diversify from Russian oil and gas imports.