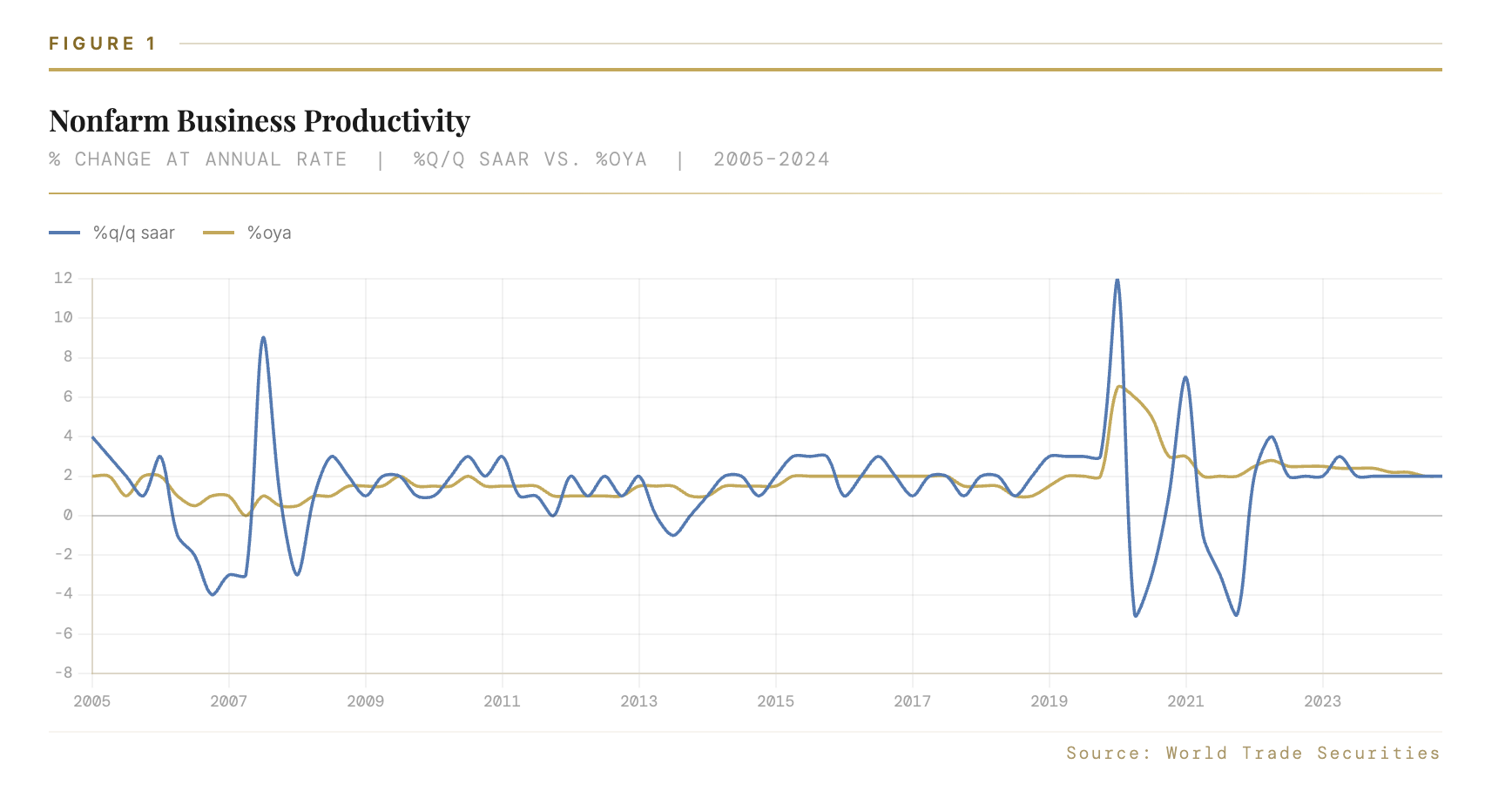

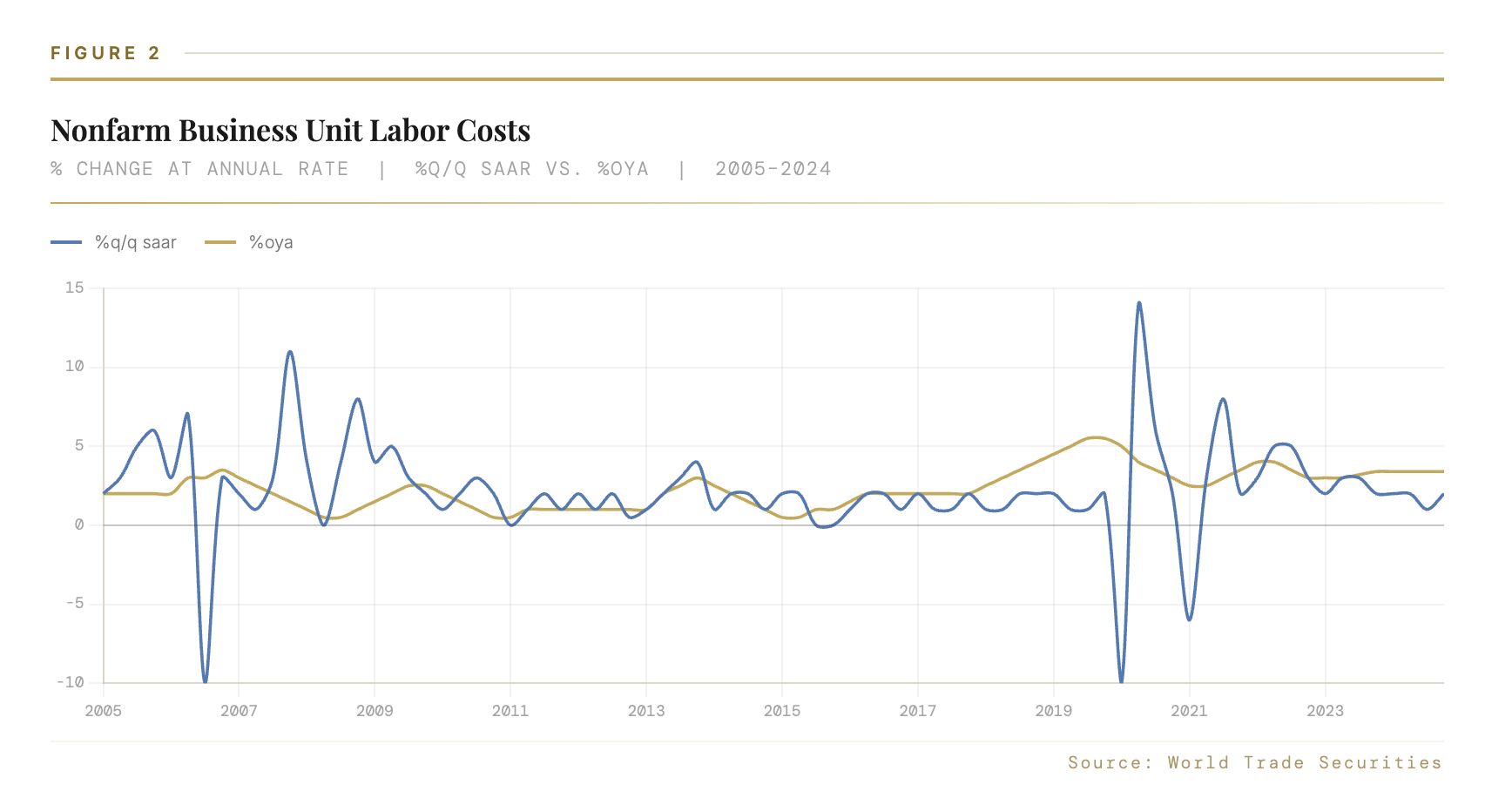

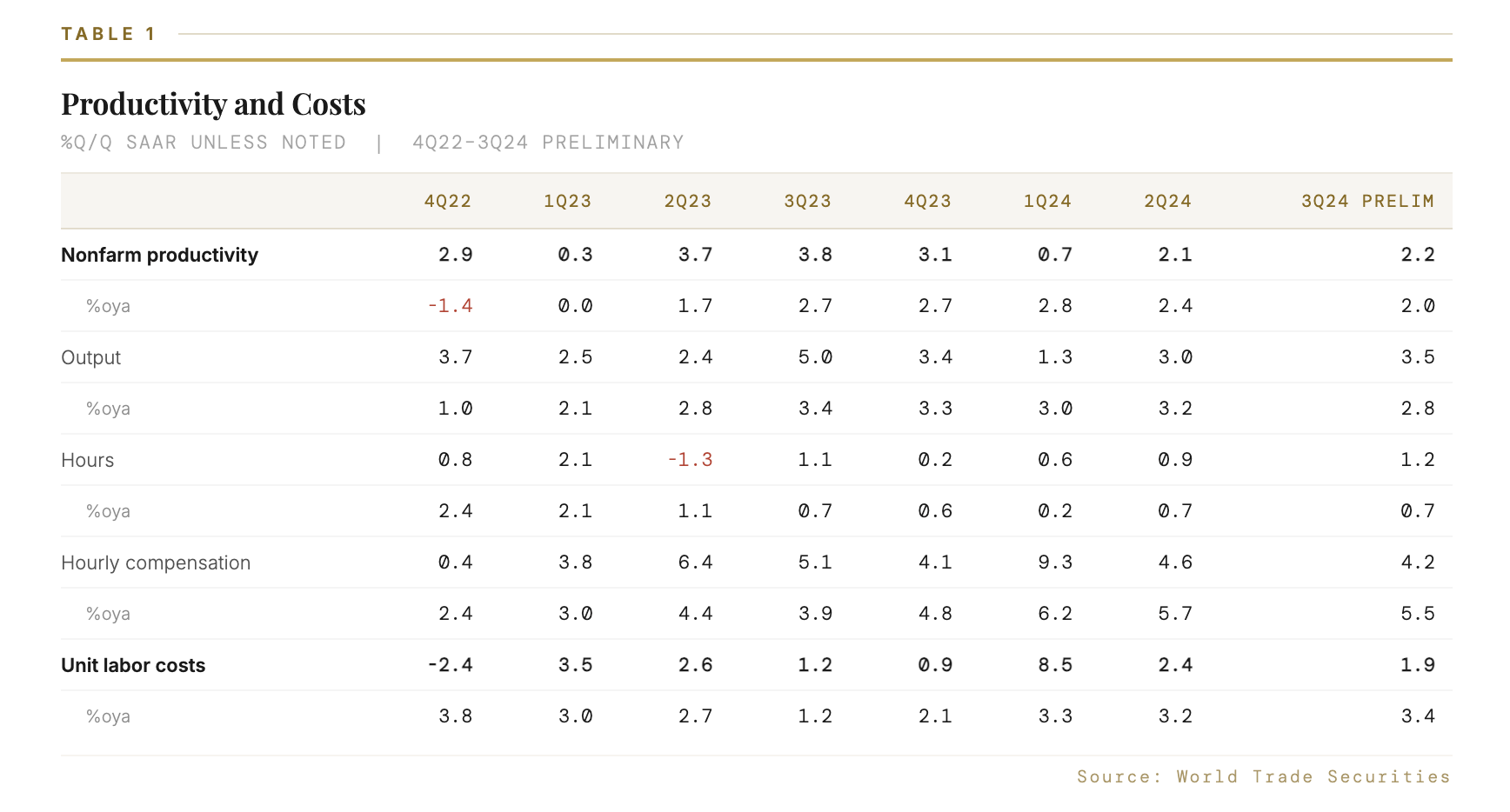

3Q productivity solid, if hints of slowing

Non-farm business productivity in 3Q rose a less-than-expected 2.2% q/q saar, while unit labor costs (ULC) rose a somewhat stronger 1.9% q/q saar last quarter. These data tend to be quite volatile from quarter to quarter, and looking at year-ago growth rates can give a smoother picture of the underlying trends. Those figures suggest productivity growth has cooled to a 2.0% pace from a mid- to upper-2% run rate over the prior several quarters, which largely reflects a downshift from annualized quarterly growth at or above 3% from late 2022 through the end of last year. But 2% is still a solid pace of productivity growth — certainly relative to the decade prior to the pandemic — and it suggests continuing supply-side supports to recent US economic growth.

Slightly more concerning, at least at first glance, is the rising trend for ULC, which climbed 3.4%oya in 3Q — its fastest annual pace in nearly two years. However, some of that acceleration reflects base effects from an 8.5% q/q saar surge in 1Q24 ULC after revisions (discussed below). As wage growth continues to cool and that observation falls out of the computation, ULC should return to a more benign and favorable trend. The Fed will monitor these data, but the productivity story should be broadly supportive for continued near-term easing of monetary policy

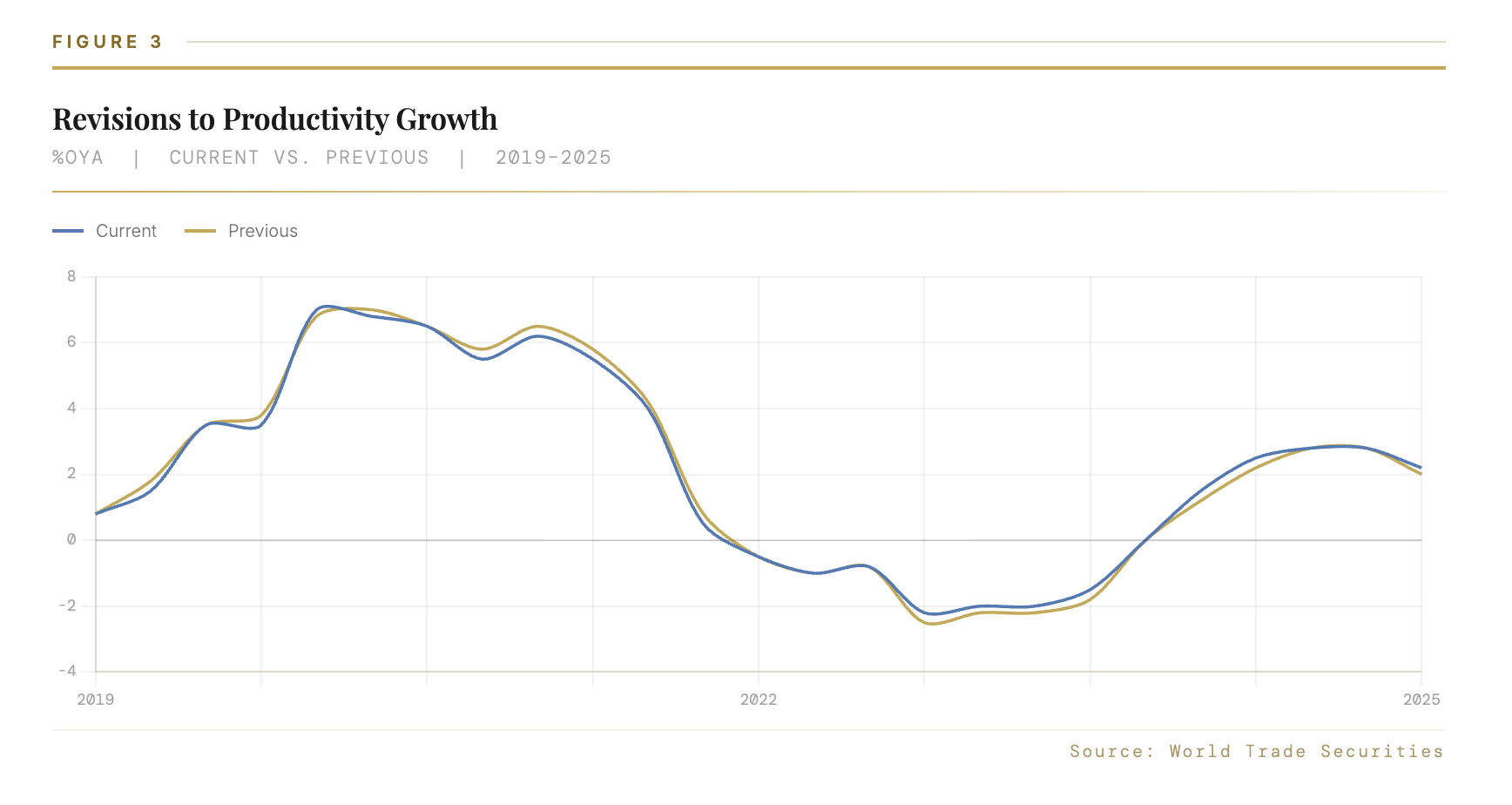

There also were revisions to the historical data with today’s 3Q report that followed from earlier benchmark revisions to the GDP data. These yielded lower values for near-term productivity growth; in 2Q, annualized non-farm productivity growth was revised down to 2.1% from 2.5% previously, with year-ago growth now at 2.4% in 2Q versus 2.7% initially. However, the historical revisions largely lifted both the index level and the growth rate of productivity for 2021 through 2023, which reinforces the idea that improvements on the supply-side of the economy have supported a continued expansion in activity and the immaculate disinflation.

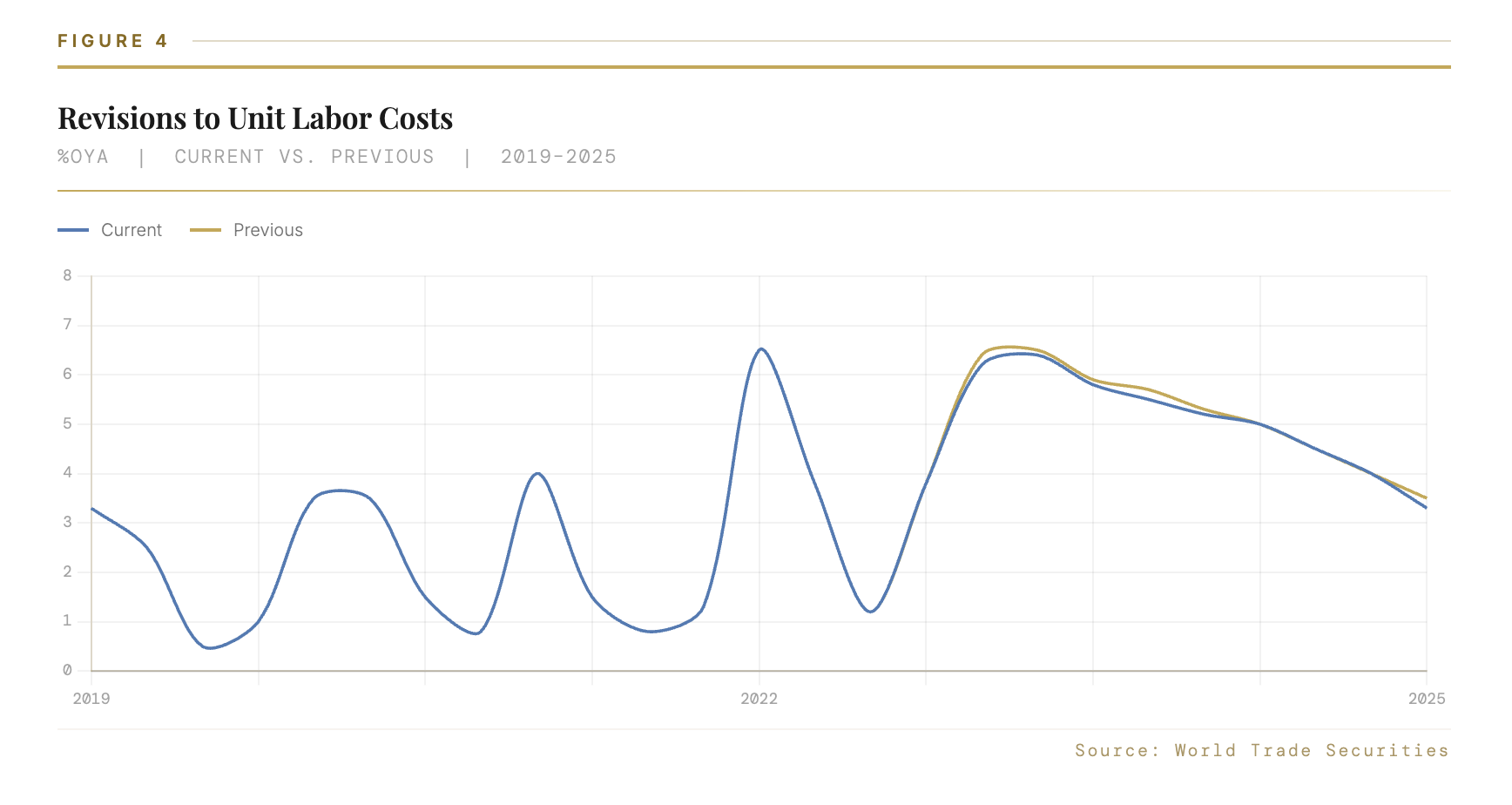

Similarly, ULC were revised marginally lower in prior years — but the big surprise was a substantial upward revision in compensation expenses that materially boosted ULC over the past year. In particular, annualized quarterly growth in 2Q ULC was revised up significantly to 2.2% from a prior 0.4% reading, with revisions surging 1Q ULC gains to 8.5% q/q saar from a prior 3.5% reading. As a result, the annual growth rate for ULC in 2Q now stands at 3.2%, which is substantially higher than the 0.3% recorded in the 2Q final release. While this paints a notably less benign picture for ULC, even the annual growth rates for this series exhibit elevated variability. We think the Fed can and will take more comfort from the slowing in wages seen in the recent 3Q ECI report, as well as signs of cooling labor demand evident during the past several months of employment reports and JOLTS data.