When I meet with clients and spend all day discussing investments and the market, I often get new ideas for memos. Last month, I met with clients in Japan — and we talked about the big shift I think is happening with interest rates and the role of credit in portfolios. This led to a broader discussion about asset allocation. I didn’t come up with a lot of new ideas, but I did find a new way to combine old ideas into a single theory.

Before I go on, I want to say that I’ll use words like “generally,” “usually,” and “everything else being equal” a lot in this memo. These words could apply to many more sentences and ideas, but I won’t repeat them over and over again. Also, I’ll use a lot of pictures, because I believe a picture is worth a thousand words. Please remember that these pictures are just for illustration, not for technical accuracy.

Asset Allocation

When I first began my career, the concept of “asset allocation” was a relatively new idea. Portfolio construction was a straightforward process, often following the classic 60/40 stock-bond split. Most investors limited their choices to domestic equities and bonds, and this balanced approach was widely considered a prudent strategy.

Today, the investment world is vastly more complex. Investors are presented with a dizzying array of choices, from traditional stocks and bonds to alternative investments like real estate, commodities, and private equity. This expanded universe of options has made asset allocation a critical decision, requiring careful consideration and strategic planning.

Asset allocators are tasked with determining the optimal allocation of assets within a portfolio. This involves making decisions such as:

- Equity vs. Debt: How much to invest in stocks versus bonds?

- Public vs. Private: How much to allocate to publicly traded securities versus private assets?

- Domestic vs. Foreign: How much to invest in domestic markets versus foreign markets?

- Developed vs. Emerging Markets: How much to allocate to developed markets versus emerging markets?

- High-Quality vs. High-Yield: How much to invest in high-quality assets versus high-yield assets?

- Growth vs. Value: How much to allocate to growth stocks versus value stocks?

- Leveraged vs. Unleveraged: How much to use leverage in investment strategies?

- Real Assets: How much to invest in real assets like real estate and commodities?

- Derivatives: How much to use derivatives for hedging and speculation?

The sheer number of choices can be overwhelming. Many investors rely on computer models to assist in decision-making, but these models often rely on historical data and assumptions that may not accurately reflect future conditions, or future prices for those *Assets*.

A fundamental distinction in asset allocation is between ownership and lending. When investing in a company, you can either:

- Own a portion of the company: This involves buying equity shares, which represent ownership in the company.

- Lend money to the company: This involves buying debt securities, such as bonds, which represent a loan to the company.

Understanding this distinction is crucial, as equity and debt investments offer different risk-return profiles. Equity investments typically offer higher potential returns but also higher risk, while debt investments generally offer lower returns but lower risk.

As our investment world continues to evolve, effective asset allocation will remain a critical driver of long-term investment success, with whatever choice an investor might make.

One of the most critical distinctions in investing, often overlooked, is the difference between ownership and lending. While stocks and bonds are often grouped together, they represent fundamentally different investment approaches.

Ownership:

- Risk: High

- Return: Potentially unlimited

- Control: Partial ownership and potential influence over the business

- Examples: Common stocks, real estate, private equity

As an owner, you share in the fortunes of a business. Your returns are tied to the company’s performance, and your investment is at risk. If the business thrives, your investment may appreciate significantly. However, if the business falters, you may lose a portion or all of your investment.

Lending:

- Risk: Lower (assuming the borrower is creditworthy)

- Return: Fixed and predictable

- Control: Limited to contractual terms

- Examples: Bonds, loans, mortgage-backed securities

As a lender, you provide capital to a borrower in exchange for a fixed return. The return is typically in the form of periodic interest payments and the repayment of the principal amount. While the risk is lower than ownership, it’s not entirely absent. If the borrower defaults on the loan, you may lose a portion or all of your investment.

Recognizing this fundamental difference is crucial for any so-called *professional investor* to not only make informed investment decisions for themselves or behalf of their clients by understanding the risk-reward trade-offs associated with ownership and lending can help non-professional investors construct portfolios that align with their financial goals and risk tolerance — which varies from investor to investor.

Risk and Reward

At the heart of successful investing lies a fundamental trade-off — risk versus reward. While many investors focus on maximizing returns, a more prudent approach involves balancing risk and reward to achieve optimal outcomes.

Risk Posture

The most critical decision in portfolio management is determining the desired risk posture. This involves deciding how much emphasis to place on:

- Preservation of Capital: Prioritizing capital protection and limiting downside risk.

- Growth: Maximizing long-term returns, even if it means accepting higher volatility.

It’s extremely important to recognize that these two objectives are often at odds. A focus on capital preservation may limit upside potential, while a focus on growth may expose the portfolio to greater risk.

The Optimization of Risk and Reward

The goal of asset allocation should be to optimize the portfolio’s risk-return profile. This involves:

- Selecting assets that offer attractive risk-adjusted returns.

- Spreading investments across various asset classes to reduce risk.

- Periodically adjusting the portfolio to maintain the desired asset allocation.

By carefully and intentionally considering these factors, investors can construct portfolios that align with their risk tolerance and financial goals!

The Importance of Risk Management

Risk management is perhaps the most important aspect of asset allocation. Investors should not only seek high returns but also ensure that the level of risk is appropriate and well-compensated. A portfolio with excessive risk may lead to significant losses, even if it offers the potential for high returns.

Ultimately, the “Secret Sauce” to successful investing lies in finding the right balance between risk and reward.

The Shape of the Curves

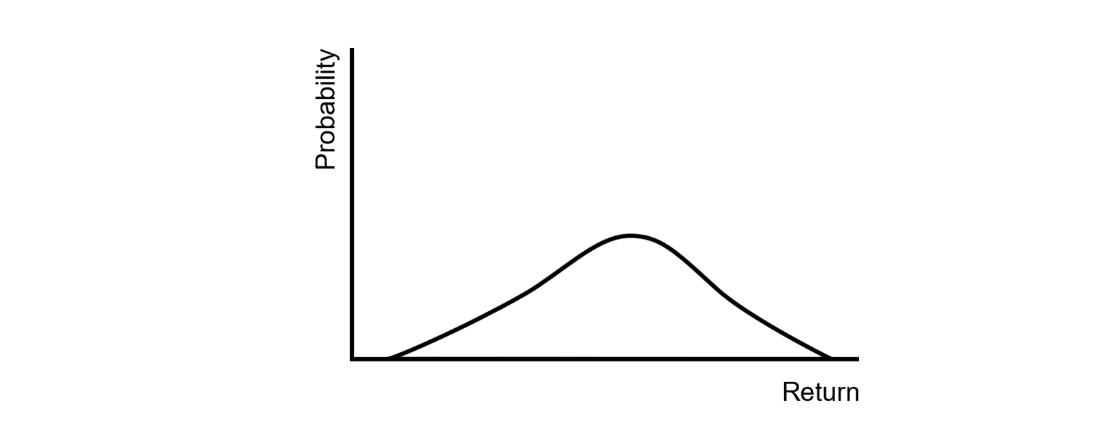

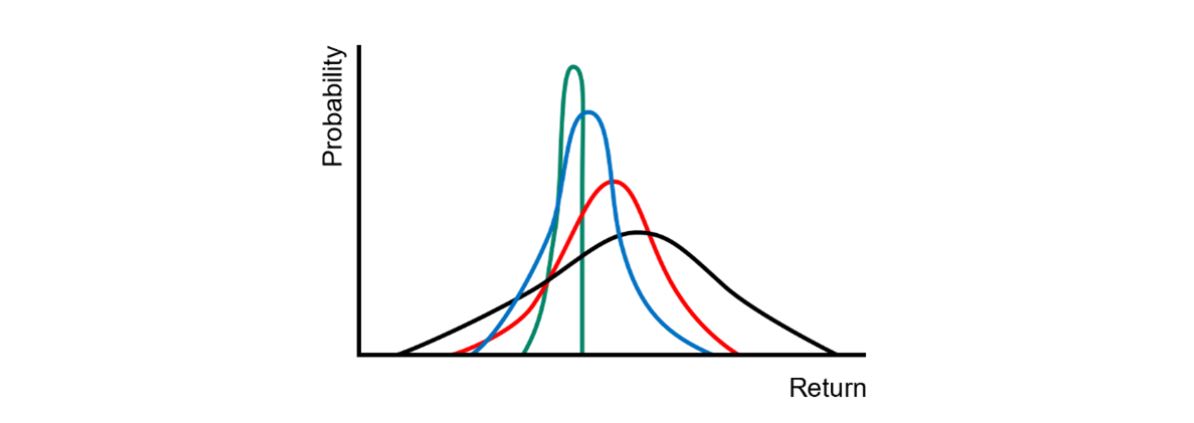

To better understand the potential returns from ownership assets and debt, I’ve been visualizing probability distributions. Let’s start with the curve for ownership assets.

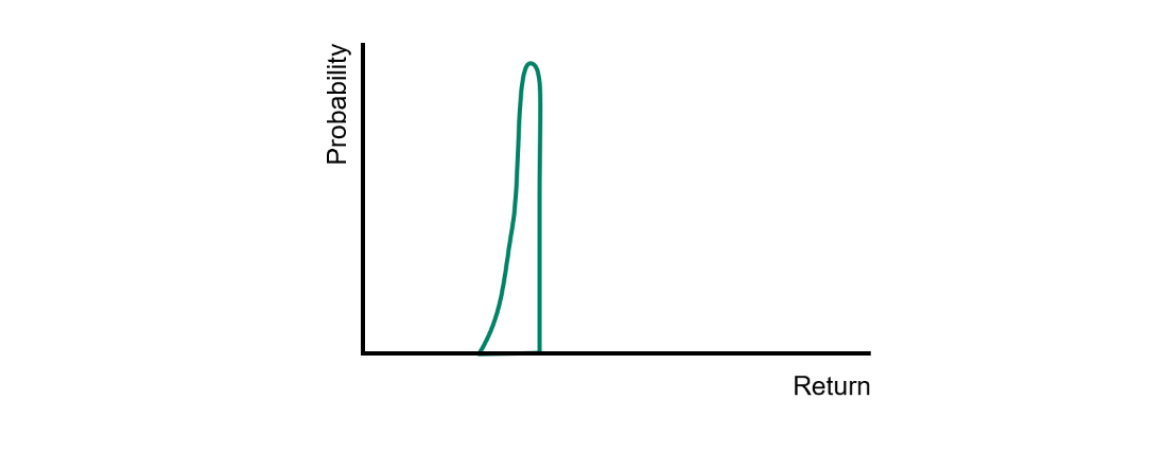

And following is the shape of the curve describing the potential return on a portfolio of debt:

Ownership assets typically offer higher expected returns but also come with greater risk.

This means that while there’s a potential for significant upside, there’s also a risk of substantial losses. The probability distribution for ownership assets reflects this wide range of potential outcomes.

On the other hand, debt investments generally offer lower expected returns but also lower risk. The probability distribution for debt is narrower, indicating a tighter range of potential outcomes. While the upside potential is limited, the downside risk is also relatively low.

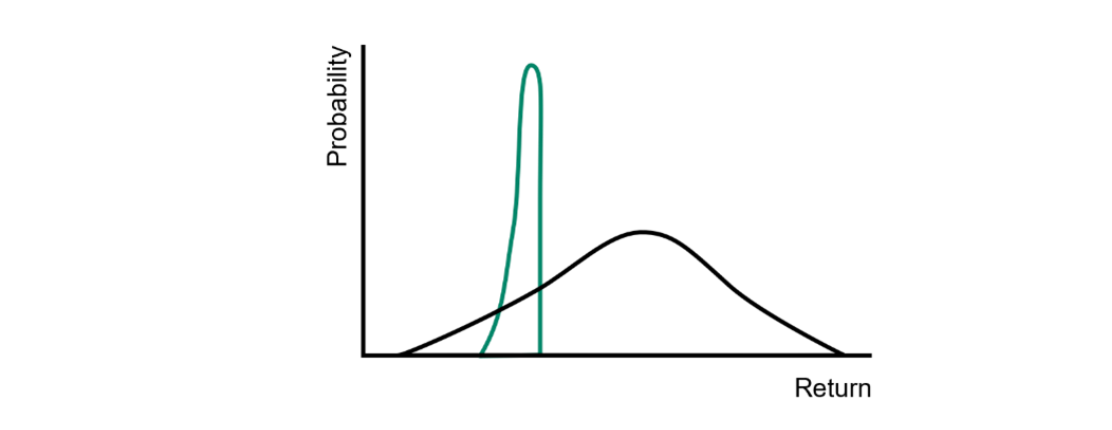

But today, the expected return on debt has increased significantly, bringing it closer to the level of equities. This shift in the risk-reward trade-off makes credit investments more attractive.

The relationship between the two curves at a specific point in time directly influences the optimal asset allocation strategy.

Neither ownership nor debt is inherently “better.” In an efficient market, the choice between the two is a trade-off:

- Ownership: Higher potential returns, but also higher risk and volatility.

- Debt: Lower, more predictable returns, with lower risk.

The ideal choice depends on the investor’s circumstances, risk tolerance, and financial goals. Some investors may prefer the higher potential returns of ownership, while others may prioritize the stability and lower risk of debt. Ultimately, the best approach involves a balanced portfolio that aligns with the investor’s specific needs and objectives.

Balancing Offense and Defense

A crucial step in asset allocation is determining the appropriate risk posture, or offense/defense balance. This decision should be based on various factors, including:

- Long-term investors may be more willing to tolerate risk.

- Net worth, income, and debt levels can influence risk tolerance.

- Personal comfort with market volatility.

Once the desired risk posture is established, investors can choose between two approaches:

- Maintaining a consistent level of risk over time.

- Adjusting the risk level in response to market conditions.

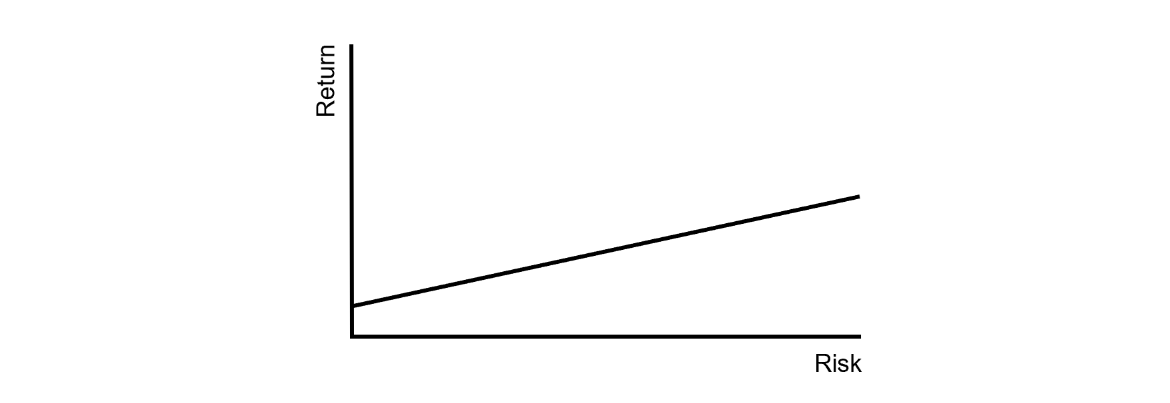

The Risk-Return Trade-off

The relationship between risk and return is a fundamental concept in investing. As risk increases, so does the potential for higher returns. This relationship is often depicted graphically as an upward-sloping line.

The traditional risk-return curve suggests a linear relationship between risk and return, implying a certain outcome. However, this oversimplifies the complex and uncertain nature of investing.

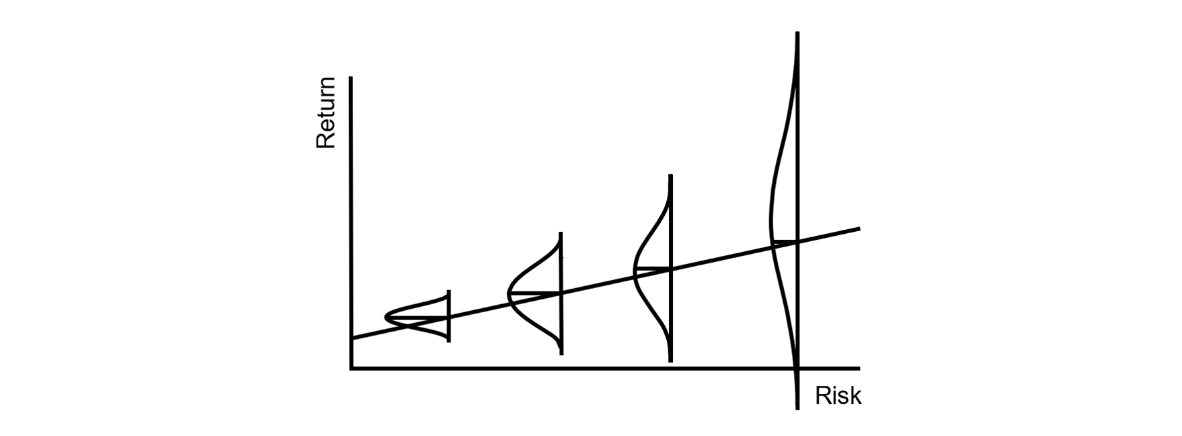

To better illustrate this point, I introduced a modified version of the risk-return curve in 2006. This revised curve incorporates probability distributions to highlight the uncertainty associated with different levels of risk.

As we increase the level of risk in an investment, we not only increase the potential for higher returns but also the potential for greater losses. This is the fundamental nature of risk. By visualizing this concept, we can better understand the trade-off between risk and reward.

To illustrate this, let’s consider the risk-return profiles of different asset allocations. We can combine ownership assets and debt in various proportions to create portfolios with different levels of risk and return:

- Conservative Portfolio: A portfolio with a higher allocation to debt and a lower allocation to ownership assets would have a lower expected return but also lower risk.

- Aggressive Portfolio: A portfolio with a higher allocation to ownership assets and a lower allocation to debt would have a higher expected return but also higher risk.

The visual representation of the risk-return trade-off – offers a clearer understanding of how different asset allocations impact potential outcomes. As we shift towards a higher proportion of ownership assets, the expected return increases, but so does the potential for significant losses. This reinforces the idea that higher risk does not always translate to higher returns.

Many investors mistakenly believe that taking on more risk will inevitably lead to higher returns. However, a deeper understanding of the risks involved can lead to a more moderate approach. By carefully considering the potential downsides of excessive risk-taking, investors can make more informed decisions about their asset allocation and ultimately (hopefully) avoiding heavy losses.

The Role of Alpha and Beta

The concept of market efficiency suggests that all assets are priced fairly, and there are no opportunities to consistently outperform the market. In such a market, the only factor that differentiates investments is their level of risk, or beta. As risk increases, so does the expected return.

However, in reality, markets are not perfectly efficient. There are opportunities for skilled investors to identify mispriced assets or employ superior strategies to generate excess returns, known as alpha.

But, while the pursuit of alpha is a common goal among investors, it is not easy to achieve. Many managers who claim to have alpha-generating abilities may not deliver on their promises. Therefore, it’s important to carefully evaluate the track record and investment process of any manager before entrusting them with your money.

In today’s investment world, non-investment grade credit offers an attractive opportunity for investors seeking a balance between risk and return. This asset class, which includes high-yield bonds and private credit, provides several key advantages:

- The current yield on non-investment grade credit is significantly higher than historical levels, making it a compelling alternative to equities.

- The contractual nature of credit investments offers a degree of stability compared to the more volatile equity market.

- Adding non-investment grade credit to a portfolio can help diversify risk and improve overall performance.