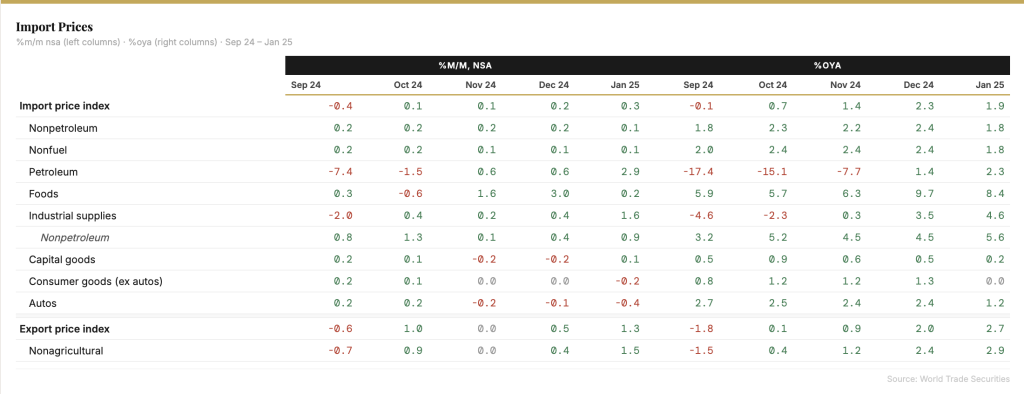

- Import prices rose 0.3% overall and 0.1% excluding fuels, pointing to some softening in their year-ago growth

- Imported energy prices, especially for natural gas, continued to climb…

- … but prices of imported manufactured goods fell despite expectations for pressure from pre-tariff front-loading

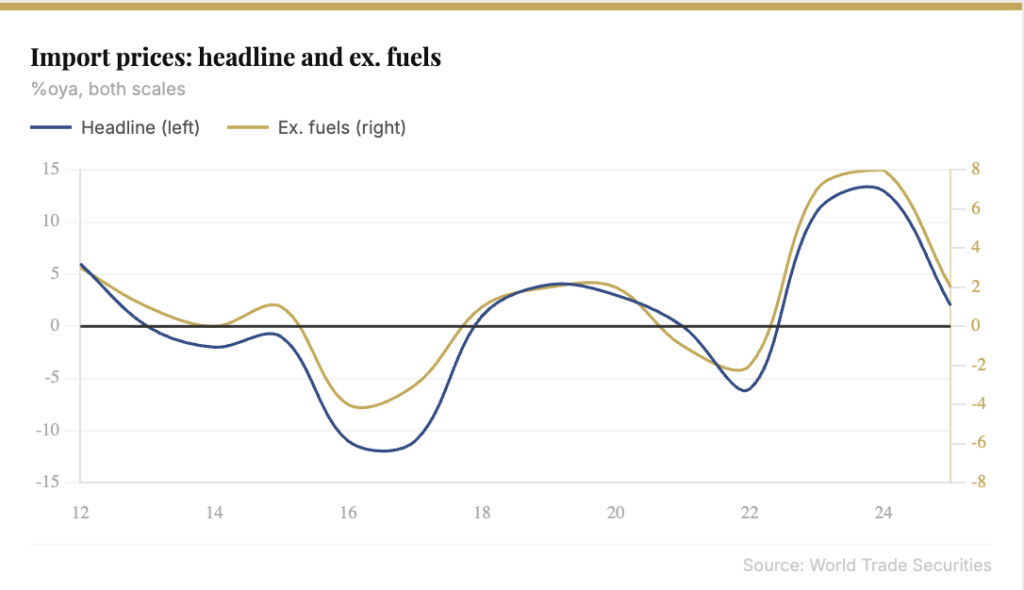

In contrast with other January inflation data this week, import prices came in slightly softer than expected. The headline measure rose 0.3% last month, but unlike most other inflation data these are not released as seasonally adjusted. On a year-ago basis, import prices grew 1.9% in January, down from an upwardly-revised 2.3% in December but still near the higher end of its range over the past two years; a year-ago import prices had been contracting at a -1.3% annual pace. Much of those dynamics can be attributed to imported energy prices; the ex-fuels import price index cooled to 1.8%oya from 2.4% in December, on a 0.1% monthly rise.

Following the trifecta of January inflation this week, which saw unexpected strength in CPI and a firm PPI—but softer readings for the individual series that matter for the core PCE price deflator—we are tracking a 0.24% m/m rise in core PCE prices for January, which would bring the annual inflation rate for this series down to 2.5% from 2.8% in December. This pace of underlying inflation appears well aligned with our expectation for the Fed to remain on hold at upcoming meetings, a position that was reinforced by Chair Powell’s testimony earlier this week as well as comments by other Fed officials.

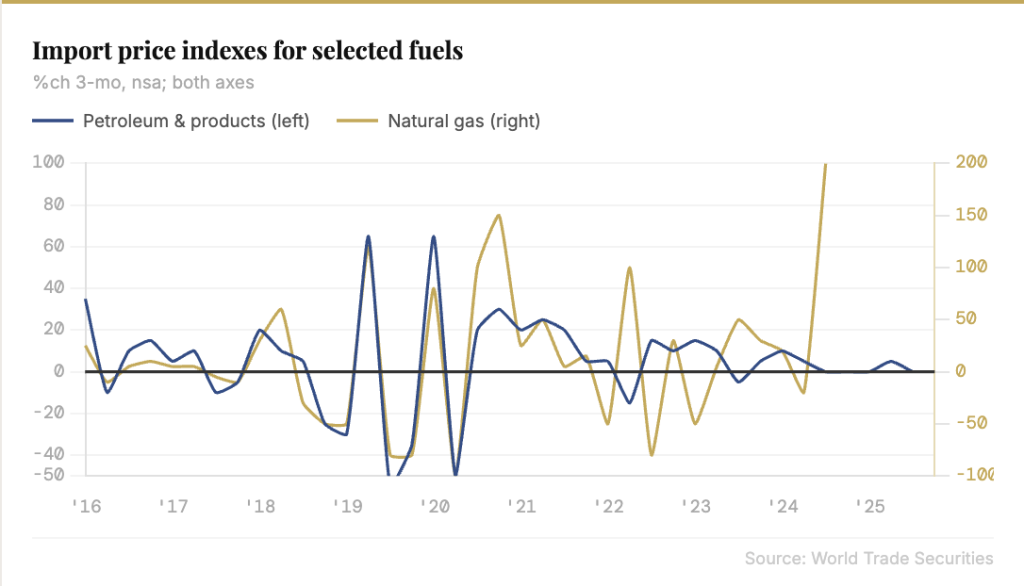

Within the details of the import prices report, as noted energy prices have been a notable add recently. While petroleum prices have been volatile over the past few years—and a notable drag on overall import prices a year ago—petroleum prices rose 2.9% on the month in January and are up 2.3% over the past year. Imported natural gas prices continued their sharp move higher, up 13.4% last month, but did not jump quite as much as in each of the prior three months. After running deeply in negative territory on a year-ago basis for more of 2023 and 2024 (imported natural gas price spiked even more throughout 2022 into early 2023, but were running at -70%oya last January), they are currently up 12.9%oya. As noted above, the ex-fuels import price index ticked higher by a tenth last month.

Outside of energy, prices of imported manufactured consumer goods fell on the month, with a sizable -0.4% drop in the import price index for motor vehicles and parts. This marked the third straight month of decline in this series, and helped sharply drop the year-ago inflation rate for imported vehicles and parts to 1.2% in January from 2.4% in December. Similarly, prices of imported consumer goods excluding autos declined -0.2% in January after flat readings for the prior two months. That also resulted in a sharp slowing of year-ago inflation for this component: it stood at 0.0%oya in January from 1.3% in December. Import prices for capital goods bucked this near-term trend by rising 0.1% in January after two months of bigger declines; but the year-ago pace of price growth also cooled to 0.2%oya from 0.5% in December for imported capital goods.

While it has been thought that the threat of US tariffs might push up near-term demand for imports, and with it prices, there is little sign of that in the recent data. Indeed, an alternative interpretation is that importers were willing to rush goods into the US ahead of potential tariffs — or had already done so, and inventories are now high. While inventory data is lagged, there has been limited signs of a big build up so far, while more recent trade data point to some potential front-loading of imports. Still, the behavior of import prices in this context is somewhat puzzling, unless importers are concerned that consumers will be very price sensitive to tariffed goods and could significantly reduce their demand in response.