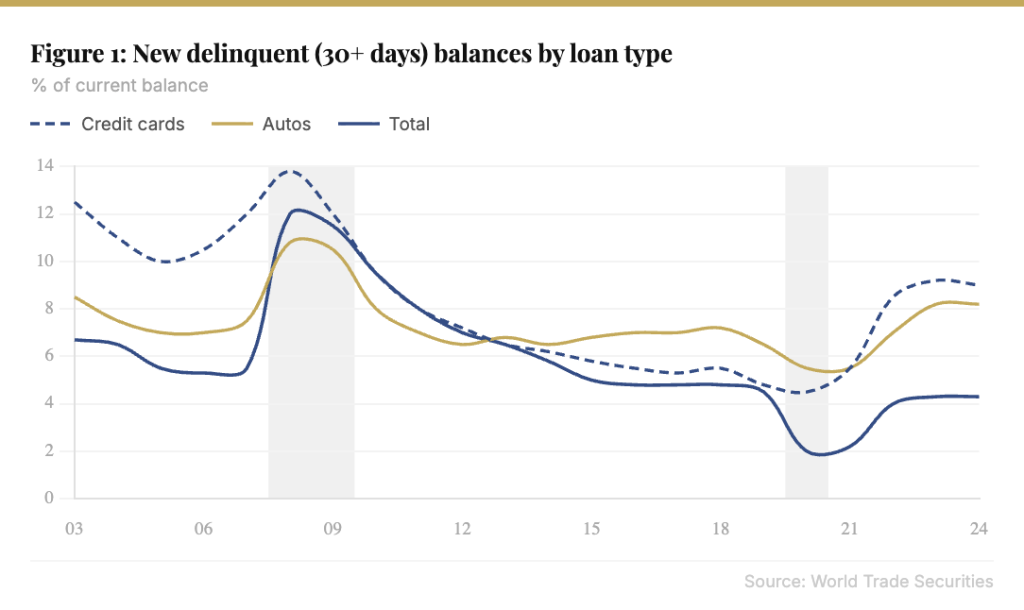

In our 2025 Outlook we highlighted how strong consumer balance sheets have been supporting spending. While real PCE growth surged over 4% in 2H24, we look for consumer spending in 1H25 to normalize to above 2% given the still solid labor market. Rising delinquencies had led to some questions about the health of consumers, but the latest 4Q household debt and credit report from the NY Fed shows delinquency rates for credit cards and auto loans have stabilized (Figure 1). However, credit bureaus were not reporting student loan delinquencies through 4Q24, which may be biasing the overall delinquency rate lower. As delinquency flags appear in credit reports, borrowers could face rising credit constraints that risk a drag on consumer spending.

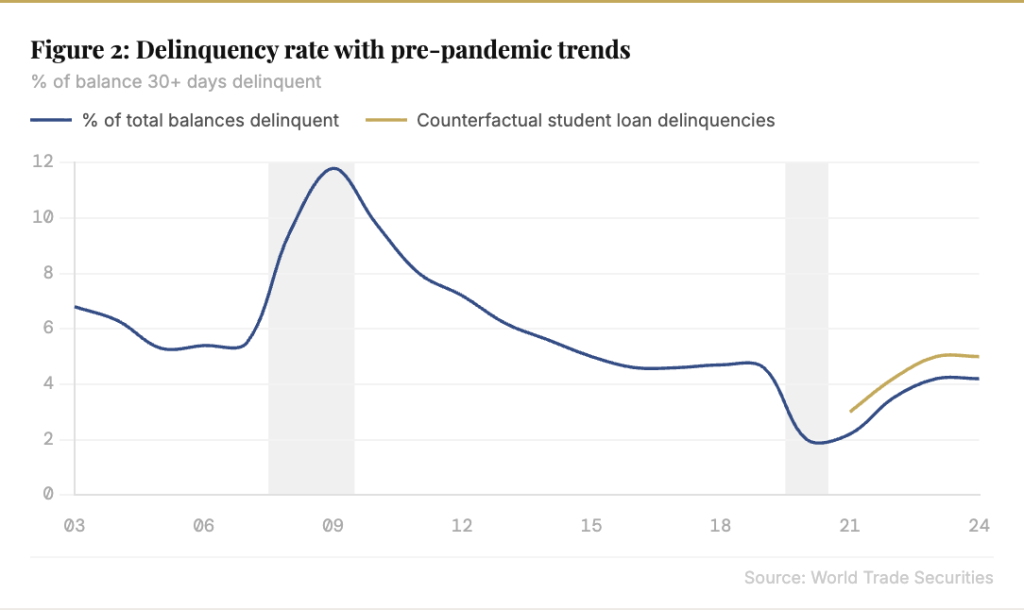

Of $18 trillion in outstanding debt, over 4.1% was newly delinquent in 4Q, up from a recent low of 2% but still below its pre pandemic level. Student loan debt reached $1.62 trillion, with only about 0.9% delinquent—a historic low—as missed payments had not been reported from 2Q20 until recently. Had the pre-pandemic historical average of about 10% for student loan delinquencies been included in the overall figures, the total recorded delinquencies would have been around a full percentage point higher, and now above their pre-pandemic level (Figure 2).

Now that credit reports are starting to reflect actual student loan delinquencies, we expect a jump in reported delinquencies this year. Recent news reports indicated that a Department of Education memo issued during the final days of the Biden administration suggested that about 5.5 million federal student loan borrowers, or over 12%, were in serious delinquency already. This represents an upside risk to our 10% baseline used for the above counterfactual.

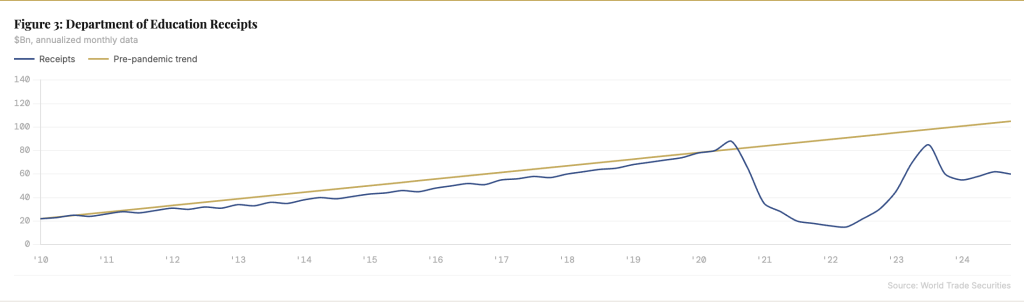

We lack sufficient data to assess how much borrowers were paying down their student loan debt during the forbearance period or over the last year since it ended. Research has showed that most direct borrowers made no payments during the pandemic forbearance. Although deposits at the Department of Education rose after forbearance ended—which we had interpreted as a preemptive effort to pay down some student loan debt—those have since moderated (Figure 3).