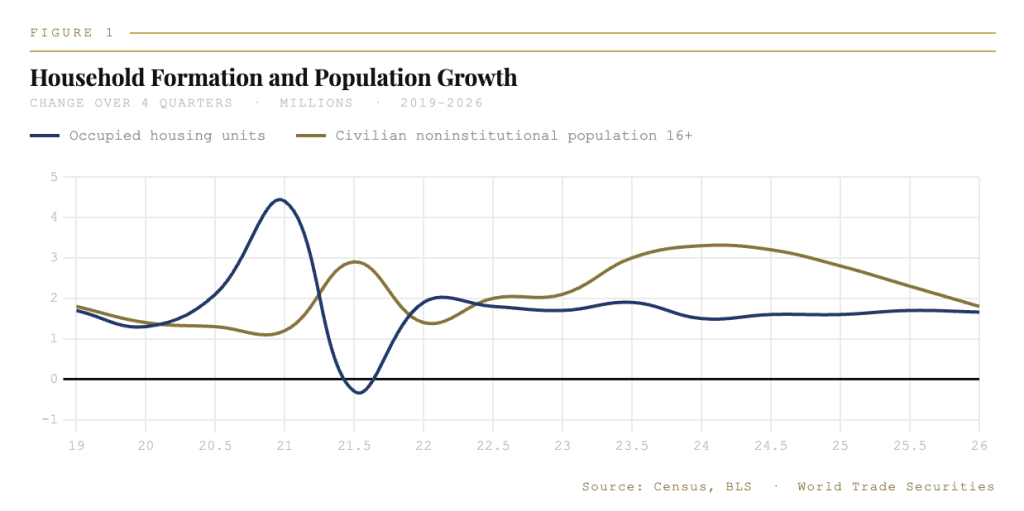

Census Bureau residential vacancies and homeownership data released this week showed total occupied housing units rising by 1.66 million over the four quarters through 1Q26 — the firmest increase since 3Q24. The pickup is counterintuitive against a backdrop of slowing population growth, which should, all else equal, represent a headwind to housing demand. The explanation lies in the headship rate.

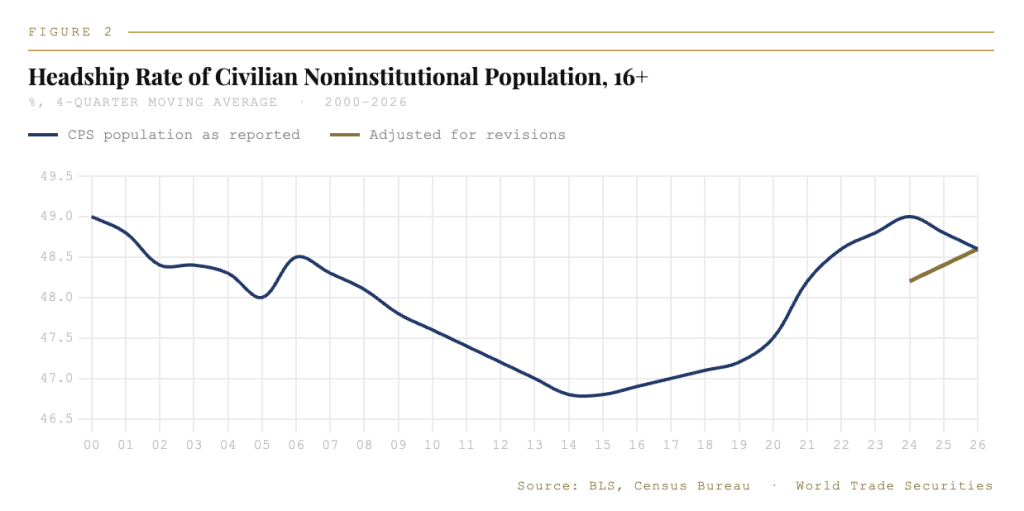

The headship rate — total occupied housing units divided by the civilian noninstitutional population aged 16+ — climbed to 48.6% on a four-quarter moving-average basis in 1Q26, a high for the period over which the adjusted series is available. The rate rose in the years immediately following the pandemic as household formation benefited from low mortgage rates, geographic mobility, and accumulated savings. It then began to lose altitude as these tailwinds faded and as a surge in net immigration from 2022 to 2024 expanded the adult population with a cohort whose propensity to form independent households is structurally lower than the broader population. The more recent return to a higher headship rate reflects the reversal of that immigration surge — a compositional tailwind we expect to persist as net inflows run well below the 2022–2024 pace under the current administration’s enforcement posture. Updated CBO projections estimate household formation of 1.2 million for full-year 2026, up from 1.1 million in 2025, even as population growth slows.

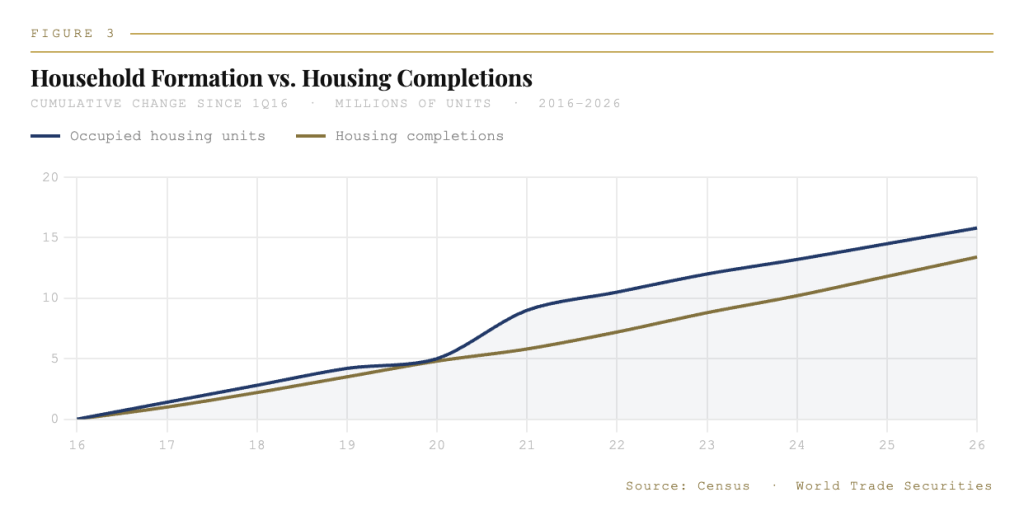

With household formation remaining firm, new supply is unlikely to close the persistent structural deficit. Over the last ten years, cumulative household formation has outpaced completions by 2.3 million units — a gap that materially understates cumulative underbuilding once the 300,000–600,000 units lost annually to demolition and obsolescence are accounted for. The supply picture shows limited signs of improvement. Housing starts are running at an annualized pace of 1.42 million units in the three months through March, modestly above the 1.35–1.37 million range that prevailed through 2024 and 2025, but the accompanying permits data were softer and builder surveys suggest persistent caution. With higher energy prices from the Middle East conflict feeding into building material costs, we expect starts to downshift in the coming months.

The structural conclusion is unchanged: housing demand is more durable than the population headline implies, and the supply response remains insufficient to normalize vacancy rates. Any additional units brought to market are likely to draw households out of doubled-up living arrangements before they can meaningfully relieve vacancy pressure. The path to equilibrium is longer than the current construction pace suggests, and the rate environment — with the Fed on hold through 2027 — provides no relief on the demand side for first-time buyers. The housing shortage is not resolving. It is compounding.