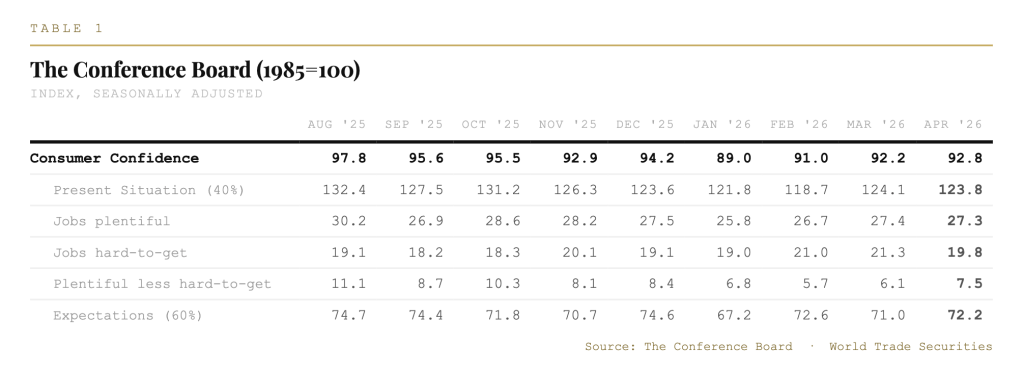

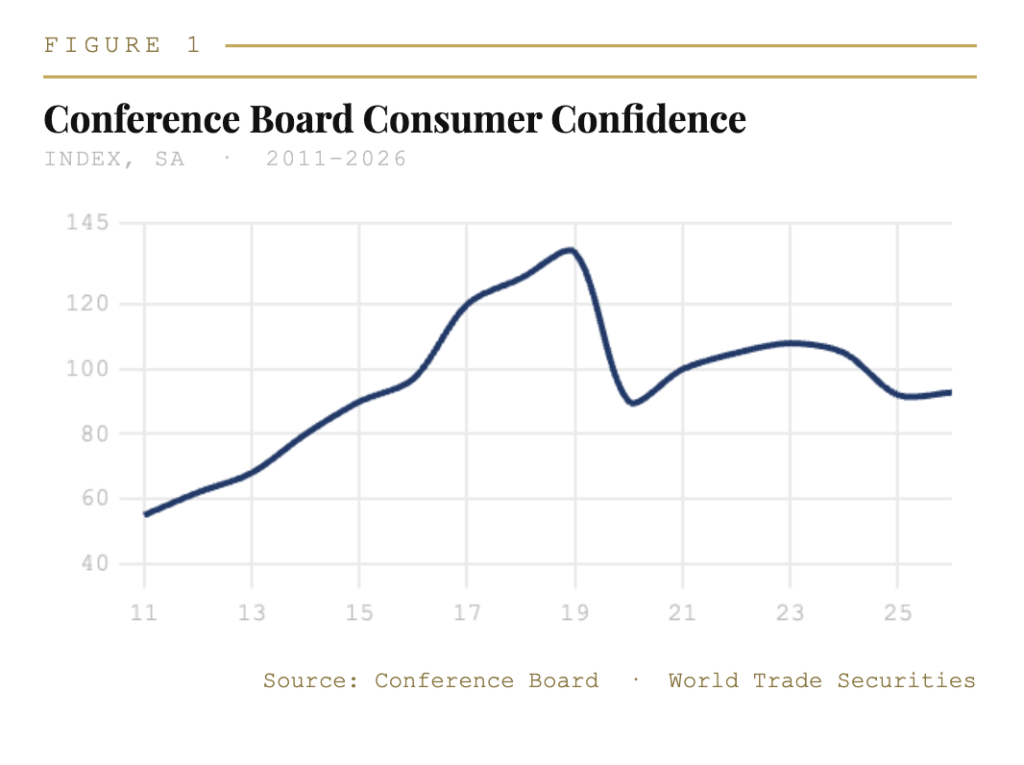

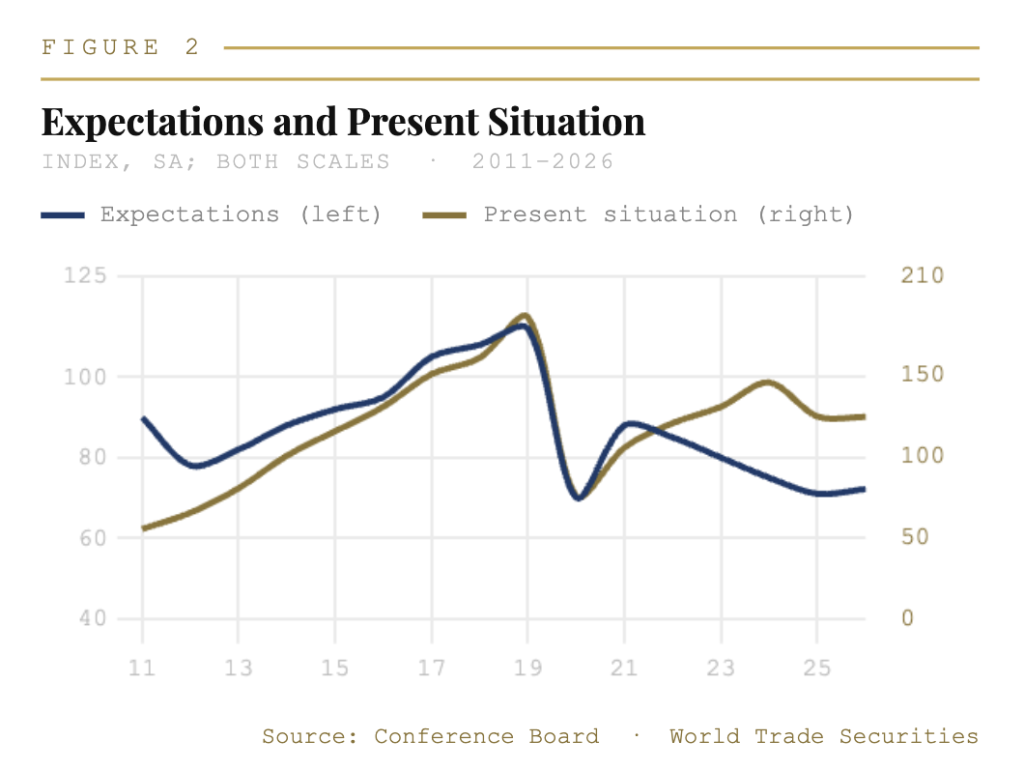

The Conference Board consumer confidence index surprised to the upside in April, rising to 92.8 from an upwardly revised 92.2 in March. The improvement was led by a rebound in the expectations component, which rose 1.2 points after sliding 1.6 points the prior month. The survey’s gauge of current conditions edged down just 0.3 points in April but is up 5.1 points over the past two months — a trend that, taken in context, represents a modest but genuine stabilization from the confidence trough of January.

The most significant development in the April release was the labor market differential, which perked up to a four-month high of 7.5% — the net share of respondents viewing jobs as plentiful relative to hard-to-get. The March reading was revised upward from 5.8% to 6.1%. This improvement carries meaningful analytical weight. The differential had been declining toward its cycle low in February in a manner that, taken alongside other labor market indicators, raised the prospect of a more pronounced rise in the unemployment rate. The April rebound, and the upward revision to March, substantially reduce that risk. Continuing claims — historically a reliable leading indicator of the unemployment rate — have also been sending a constructive signal, together suggesting that the unemployment rate is likely to remain in the low-4% range in the near term.

Beneath the headline, the composition of the April report reflects the unusual cross-currents facing consumers. Deterioration in views of current business conditions was partially offset by improving perceptions of employment availability. Forward-looking assessments of business conditions six months out were modestly more negative than in March, while an improved labor market and household income outlook drove the rise in the overall expectations index. The Conference Board noted in its press release that the survey-sample period of April 1–22 captured both a two-week ceasefire announcement in the Middle East conflict and a partial rebound in equity markets, conditions that likely provided some temporary support to financial sentiment after the sharp deterioration recorded in March.

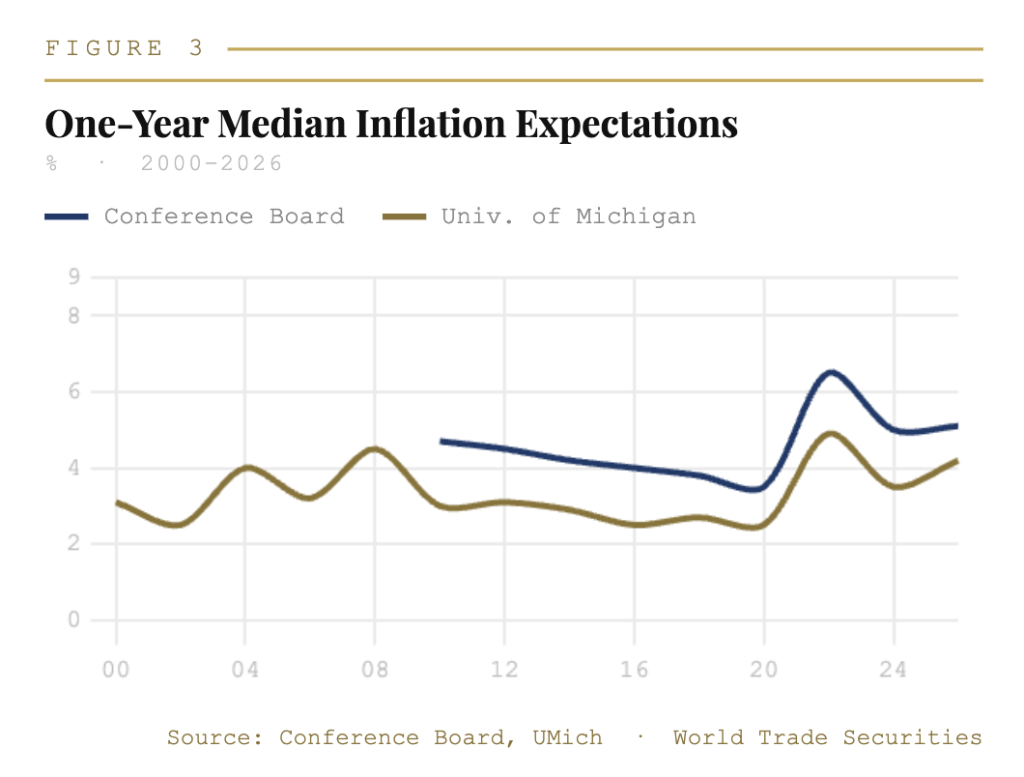

The inflation picture offers less comfort. Consumers’ median one-year inflation expectations held at 5.1% in April, declining by only a tenth from March. 49% of respondents on net expect higher interest rates over the next twelve months, up from 43% in March — a marked upward shift that is consistent with the view that households have not yet internalized a disinflationary trajectory, and that the Fed’s on-hold posture will face continued political and market scrutiny. At 5.1%, the Conference Board’s one-year inflation measure sits well above the University of Michigan’s corresponding series and materially above the Federal Reserve’s 2% target. That gap between realized PCE, stated inflation expectations, and the Fed’s mandate is the central tension in the current policy environment.

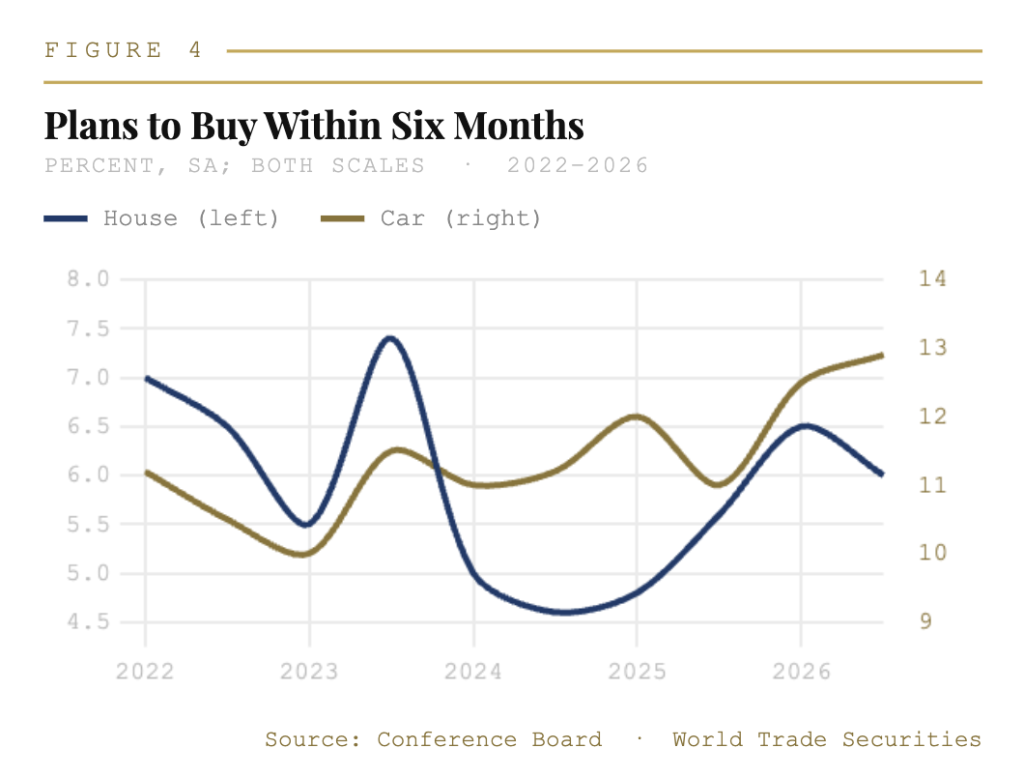

Purchasing intentions were mixed. Plans to buy a house and motor vehicle over the next six months both rose, consistent with pent-up demand from the rate-constrained environment of the past two years. Plans for a range of other big-ticket items were pulled back. The share of respondents planning a domestic vacation fell to a fourteen-month low of 37.5% — a data point that deserves attention as a leading indicator for leisure spending. Plans for foreign vacations partially recovered to February levels following the ceasefire news, suggesting that geopolitical risk remains an active variable in household decision-making rather than a background condition that has been fully discounted.

On balance, April’s Conference Board data represent a stabilization rather than a recovery. The headline index at 92.8 remains well below its pre-tariff-shock levels of late 2025 and consistent with a consumer that is functioning but operating under constraint. The labor market signal is the one unambiguously positive development, and it is the variable that matters most for the consumption outlook. As long as the unemployment rate holds in the low-4% range — as the differential and continuing claims data suggest it will — the consumption base remains broadly intact, even as confidence remains subdued and inflation expectations stay elevated.